Business Valuation Services

Table of Contents

Understanding Business Valuation Services

Business valuation services play a pivotal role in mergers and acquisitions transactions, providing precise assessments of a company’s economic value to guide strategic decisions. These services employ standardized methodologies to determine enterprise worth, ensuring stakeholders in corporate clients and private equity firms can navigate complex deals with confidence. At Zaidwood Capital LLC, we integrate these valuations seamlessly into our full-cycle M&A advisory and capital formation processes.

Determining a company’s value involves rigorous analysis using approaches like income, market, and asset-based methods, as outlined in foundational principles from IRS business valuation guidelines. This process is essential for buy-side and sell-side mandates, informing negotiations, due diligence, and capital raising efforts. For private equity firms, accurate company valuation assessments enhance deal sourcing, mitigate risks, and support liquidity solutions or growth equity pursuits. As a zaidwood capital advisory firm, we leverage our network of over 4,000 investors and access to $15 billion in deployable capital, backed by a proven track record of $24.4 billion in transaction volume, to deliver valuation-driven insights that streamline transactions.

This guide explores key business valuation methods, influencing factors, typical timelines, and criteria for selecting business valuation firms. We delve into practical applications for M&A scenarios, equipping you with the knowledge to make informed choices.

Building on these essentials, the following sections outline the fundamentals of valuation processes and their strategic implications in today’s dynamic markets.

Core Fundamentals of Business Valuation

At Zaidwood Capital, we recognize that business valuation services form the cornerstone of informed decision-making in mergers and acquisitions. These assessments determine a company’s worth by evaluating its economic value, crucial for private equity and corporate clients navigating complex transactions. Whether preparing for a sale or strategic partnership, understanding these fundamentals ensures alignment with full-cycle due diligence and advisory needs. For instance, when considering Business Valuation For Sale, clients benefit from methodologies that reflect true market potential.

Several core factors influence business valuations, particularly in M&A contexts. We recommend considering financial performance, which includes revenue trends, profitability margins, and cash flow stability to gauge operational health. Market conditions play a vital role, encompassing economic cycles, interest rates, and competitive landscapes that affect buyer appetite. Industry trends, such as technological disruptions or regulatory shifts, further shape projections.

- Intangible assets: Brand value, intellectual property, and customer relationships often add significant worth beyond tangible holdings, especially in knowledge-driven sectors.

Regulatory standards from the IRS and AICPA guide these evaluations, ensuring fairness and compliance in reporting. In our experience serving as one of the leading business valuation firms, these elements provide a balanced view for capital raising and deal structuring.

Business valuation methods offer structured approaches to quantify value, each suited to different scenarios. The income approach forecasts future earnings, discounting them to present value using growth rates and risk factors. The market approach compares the business to similar transactions or peers via multiples like EV/EBITDA. The asset-based approach calculates net worth by subtracting liabilities from asset values, ideal for balance-sheet focused entities.

Selecting the right method depends on the business stage and transaction type. For growing firms, income methods highlight potential, while mature ones favor market comparables.

| Method | Focus Area | Key Inputs | Best For |

|---|---|---|---|

| Income Approach | Future earnings potential | Projected cash flows, discount rates | Companies with stable revenues |

| Market Approach | Comparable market transactions | Peer multiples, transaction data | Industries with active deals |

| Asset-Based Approach | Net asset value | Balance sheet assets/liabilities | Liquidation or holding companies |

This overview illustrates primary business valuation methods and their applications. According to the AICPA PE/VC Accounting and Valuation Guide, method selection in M&A should align with fair value principles, emphasizing robust inputs for private equity investments to mitigate risks in portfolio company assessments.

In M&A transactions, these valuation techniques integrate seamlessly with our services, supporting due diligence and strategic advisory. For early-stage ventures, income approaches reveal upside potential despite volatility, while asset-based methods suit liquidation scenarios with clear balance sheets. Pros include the income method’s forward-looking insights for capital raising, though it relies on assumptions; market methods offer quick benchmarks but require active comparables. Asset approaches provide simplicity for holding companies yet undervalue intangibles. We at Zaidwood Capital apply appraisal methodologies tailored to client needs, ensuring compliance with AICPA and IRS standards for reliable outcomes in dynamic markets.

In-Depth Exploration of Business Valuation Methods

At Zaidwood Capital, our How To Value My Business process integrates essential Business Valuation Services to support clients in mergers and acquisitions. We employ a range of business valuation methods to deliver precise assessments, ensuring fair pricing and thorough due diligence for private equity transactions. These valuation methodologies form the backbone of our advisory approach, helping firms navigate complex deals with confidence.

Income Approach in Business Valuation

The income approach estimates a business’s value based on its ability to generate future earnings, making it ideal for revenue-stable firms in M&A scenarios. It focuses on projected cash flows, discounted to present value, or capitalized earnings for steady operations. Key methods include discounted cash flow (DCF) analysis and capitalization of earnings.

DCF involves forecasting free cash flows over a period, typically five to ten years, and discounting them using a weighted average cost of capital (WACC). The formula is straightforward: Value = Ì‘ (CF_t / (1 + r)^t) + Terminal Value / (1 + r)^n, where CF_t is cash flow in year t, r is the discount rate, and the terminal value captures perpetuity. According to the AICPA PE/VC Guide, DCF best practices emphasize realistic projections aligned with market conditions, particularly in private equity contexts where growth assumptions must reflect verifiable data.

Capitalization of earnings, suited for stable firms, applies a capitalization rate to normalized earnings: Value = Earnings / Cap Rate. We use this when cash flows are predictable, avoiding the complexity of multi-year forecasts. For instance, in valuing a mid-sized manufacturing firm for acquisition, DCF captures expansion potential, while capitalization suits mature operations.

| Method | Key Assumptions | Suitability in M&A |

|---|---|---|

| DCF | Detailed cash flow projections | Growth-oriented targets |

| Capitalization of Earnings | Stable, normalized earnings | Revenue-stable acquisitions |

Comparison of primary business valuation methods in M&A transactions

Market and Asset-Based Approaches Explained

The market approach values a business by comparing it to similar entities, using multiples from comparable companies or precedent transactions. This method relies on real-world data, such as price-to-earnings (P/E) or enterprise value-to-EBITDA (EV/EBITDA) ratios. For example, in a private equity buyout, we analyze recent deals of peer firms to apply a multiple, like 8x EBITDA, to the target’s earnings.

Precedent transactions, drawn from SEC filings, offer transaction-specific benchmarks. The SEC Edgar filing for Citizens Bancshares illustrates this through comparable whole bank analyses, where multiples from similar mergers adjusted for synergies yielded a fair value per share of $145.00. This approach excels in M&A for its market-driven objectivity but requires sufficient comparables, which may be scarce in niche industries.

Complementing this, the asset-based approach calculates value from net assets, either going concern (adjusted book value) or liquidation scenarios. Adjusted net assets subtract liabilities from appraised asset values, including intangibles where applicable. Liquidation value assumes asset sales at distressed prices, useful for distressed M&A targets.

In a neutral scenario, appraising an asset-rich logistics company for acquisition, we might use adjusted net assets at $50 million, incorporating equipment appraisals, while market multiples from recent sector deals add a premium for goodwill. Pros include tangibility for asset-heavy firms; cons involve overlooking earning potential. Overall, these appraisal techniques provide balanced perspectives, with market methods offering relativity and asset-based ensuring a floor value in transactions.

| Method | Pros | Cons |

|---|---|---|

| Income Approach | Forward-looking, captures growth potential | Sensitive to assumptions, complex calculations |

| Market Approach | Market-driven, easy to benchmark | Limited comparables in niche industries |

| Asset-Based Approach | Objective for asset-rich firms | Ignores future earnings, undervalues intangibles |

Pros and Cons of Valuation Methods

Each business valuation method carries distinct strengths and limitations, guiding selection in M&A contexts. The income approach shines in capturing intangible growth, as validated by AICPA standards for PE/VC, but its reliance on subjective forecasts can introduce variability–ideal for dynamic targets yet risky without solid data.

Market methods provide quick, empirical insights from precedents like those in SEC analyses, promoting efficiency. However, data scarcity in specialized sectors limits applicability, potentially skewing results.

Asset-based techniques offer concrete baselines for liquidation or asset sales, minimizing speculation. Drawbacks include neglecting operational synergies, undervaluing service-oriented firms.

Practical Applications of Business Valuation in M&A

In the dynamic landscape of mergers and acquisitions, zaidwood capital financial services play a pivotal role in providing clarity and value to transactions. Business Valuation Services form the foundation for informed decision-making, enabling companies to assess their worth accurately before engaging in deals. We at Zaidwood Capital emphasize practical strategies to integrate these services seamlessly into M&A processes, ensuring clients achieve optimal outcomes.

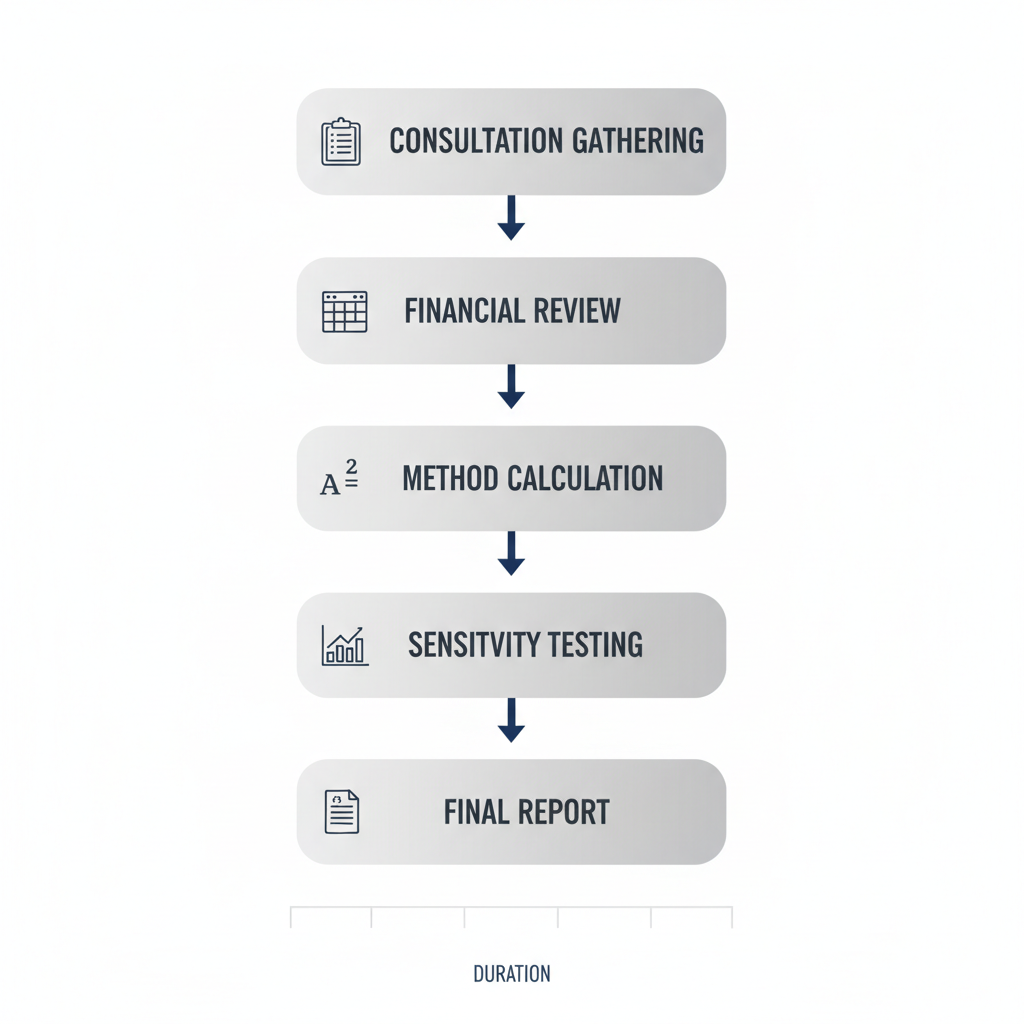

Timelines and Processes in Valuation Services

Completing a business valuation typically spans 4 to 8 weeks, depending on the complexity of the business and data availability. This timeframe allows for thorough analysis while aligning with M&A preparation needs.

- Assemble key documents upfront.

- Define valuation objectives tied to transaction goals.

- Schedule milestones for interim reviews.

Step-by-step business valuation process for M&A advisory services

Selecting a Business Valuation Firm

| Criterion | Importance for M&A | What to Look For |

|---|---|---|

| Experience in M&A | High – Ensures transaction relevance | Proven deal volume, sector knowledge |

| Cost Structure | Medium – Balances quality and budget | Fixed fees vs. hourly, transparency |

| Network Access | High – Aids capital introductions | Investor connections, transaction history |

Valuation Timing for Capital Raising

Strategic timing for valuations is essential before capital raising, ideally 3 to 6 months in advance. This allows for accurate assessments of readiness and value proposition. Integrating valuations early in M&A processes uncovers growth potential, making pitches to investors more compelling.

Advanced Strategies in Business Valuation for Private Equity

At Zaidwood Capital, we recognize the pivotal role of Business Valuation Services in empowering private equity firms to navigate complex transactions with precision. By leveraging sophisticated business valuation methods, private equity professionals can uncover hidden value and mitigate uncertainties throughout the investment lifecycle.

| Deal Stage | Valuation Role | PE Benefit |

|---|---|---|

| Sourcing | Target screening | Identifies undervalued assets |

| Due Diligence | Risk assessment | Supports informed bids |

| Exit | Fairness opinions | Maximizes returns |

Frequently Asked Questions on Business Valuation

What factors influence business valuation in M&A?

Several elements, including financial performance, market conditions, and growth potential, shape valuations. We at Zaidwood integrate comprehensive analysis to ensure accurate assessments in mergers acquisitions advisory.

How long does a business valuation process typically take?

Timelines vary from 4-8 weeks, depending on data complexity and scope. Our team streamlines this for efficient M&A timelines.

How do I select the right business valuation methods?

Choose based on business stage and purpose; income-based like DCF suits growth firms, while market approaches fit comparables. We apply tailored business valuation methods for precision.

Key Takeaways on Business Valuation Strategies

Business Valuation Services form the cornerstone of successful mergers and acquisitions, enabling private equity and corporate clients to navigate complex transactions with confidence. We have explored essential business valuation methods, including discounted cash flow and comparable company analysis, alongside critical factors like market conditions and financial projections.