Best Asset Based Lending for 2026: Top Companies Compared

Table of Contents

- Asset-Based Lending as a Strategic Financing Tool

- Understanding Asset-Based Lending Fundamentals

- Deep Dive into Asset-Based Lending Structures and Collateral Types

- Practical Guide to Securing Asset-Based Lending for Growth and Acquisitions

- Advanced Considerations in Asset-Based Lending for M&A and Complex Transactions

- Frequently Asked Questions About Asset-Based Lending

- Leveraging Asset-Based Lending with Zaidwood Capital’s Debt Advisory Expertise

Asset-Based Lending as a Strategic Financing Tool

Beyond traditional cash-flow loans, asset-based lending offers a strategic alternative for companies seeking flexible, secured financing against their balance-sheet assets. The U.S. Securities and Exchange Commission defines collateral as an asset a lender accepts as security for a loan, including real estate, equipment, inventory, and accounts receivable—precisely the assets that underpin asset-based lending structures.

Through asset-based lending, businesses can often achieve higher leverage than unsecured debt and benefit from lower interest rates because the loan is backed by tangible collateral. This approach is especially valuable for companies with strong asset bases but uneven earnings, as the financing capacity is tied to asset values rather than cash-flow metrics alone.

Qualifying typically requires a disciplined institutional process. As outlined in our FAQ, investors commonly look for collateral coverage ratios—often 1.5x to 2.0x advance rates—together with audited historical financials, minimum EBITDA thresholds, and thorough asset-quality audits. These benchmarks help our team identify the right institutional match from a network of over 4,000 investors, including banks, credit funds, and specialty finance firms.

Unlike cash-flow financing, which depends heavily on EBITDA, asset-based lending unlocks liquidity directly from receivables, inventory, equipment, or real estate. Many companies use both structures concurrently, blending them to optimize cost of capital and funding flexibility. Through our global lending services, we connect clients with institutional investors specializing in asset-based lending and other secured debt structures.

Asset-based lending can fund acquisitions, bridge equity gaps, or provide seasonal working capital—but outcomes are not guaranteed and depend on asset quality and deal structure. While many companies qualify, each transaction is subject to investor approval and due diligence.

In the following section, we explore how ABL can be structured alongside equity financing to maximize transaction efficiency.

This is not an offer or solicitation; consult your advisor.

Understanding Asset-Based Lending Fundamentals

Having defined asset-based lending, let us examine its core mechanics and how it compares with traditional financing. Asset based lending is a secured financing facility where the borrowing amount is determined by the value of specific pledged assets rather than primarily by cash flow or credit history. This type of secured lending relies on four main asset classes: accounts receivable, inventory, equipment, and real estate, each valued with distinct advance rates that reflect their liquidity and liquidation potential.

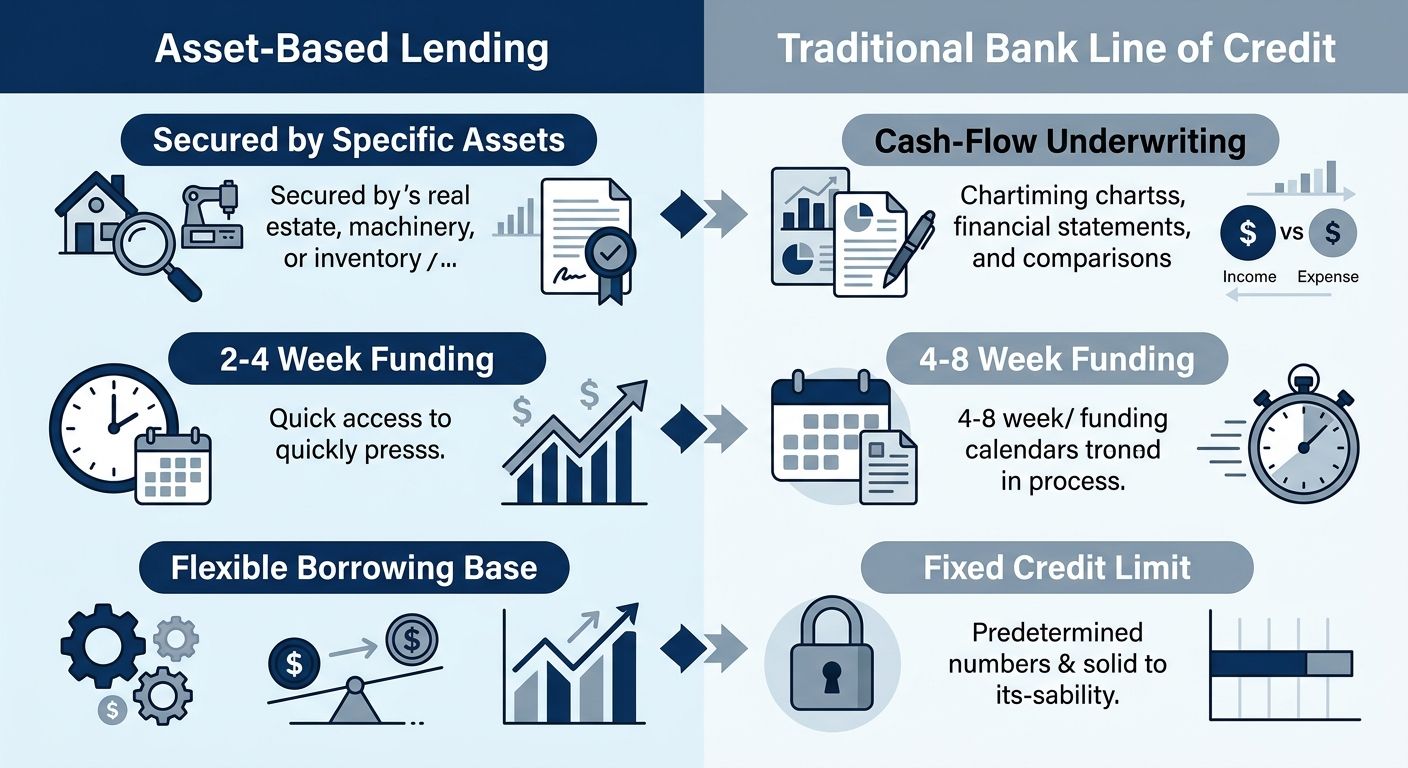

The following table highlights the key differences between asset-based lending and a traditional bank line of credit.

| Dimension | Asset-Based Lending | Traditional Bank Line of Credit |

|---|---|---|

| Collateral Requirement | Secured by specific assets (AR, inventory, equipment, real estate) | Often unsecured or blanket lien; may require personal guarantees |

| Underwriting Focus | Asset quality and liquidation value; less emphasis on cash flow | Cash flow, credit history, and overall financial health |

| Funding Speed | Typically 2–4 weeks; faster for revolving facilities | Can take 4–8 weeks or longer for approval and funding |

| Flexibility | Highly flexible; borrowing base adjusts with asset levels | Fixed credit limit; less responsive to asset fluctuations |

| Covenants | Fewer financial covenants; focus on asset reporting | Strict financial covenants (debt service coverage, leverage ratios) |

An ABL facility emphasizes the quality and liquidation value of collateral, with fewer financial covenants and a borrowing base that flexes alongside asset levels. For businesses with strong collateral but variable cash flow, such as manufacturers, wholesalers, or distributors, secured asset lending often provides faster access to capital and greater responsiveness to seasonal or growth-driven asset fluctuations.

Underwriting in asset-backed financing concentrates on the quality, liquidity, and liquidation value of the pledged collateral. Advance rates vary by asset class, with accounts receivable typically commanding higher advance rates than inventory or equipment. This approach shifts reporting toward asset monitoring rather than strict debt service coverage ratios, making ABL accessible to companies that may not meet conventional bank criteria. For a broader perspective on financing options, our coverage of global lending services alternatives provides key considerations for borrowers comparing ABL with other structures.

Deep Dive into Asset-Based Lending Structures and Collateral Types

To understand how asset based lending works, it is essential to examine the four primary collateral types that underpin every ABL structure. Each asset class carries distinct risk profiles, valuation methodologies, and advance rate ranges that directly influence the amount of capital a business can access and the speed at which funds become available.

Primary Collateral Categories and Their Characteristics

In asset based lending, collateral types determine both eligibility and borrowing capacity. The U.S. Securities and Exchange Commission defines collateral broadly as assets pledged to secure a loan, and within ABL structures, lenders focus on four principal categories based on their liquidity and ease of valuation.

Accounts receivable represent the most liquid and preferred collateral class. Lenders evaluate AR through aging reports that identify overdue invoices, dilution analysis that measures returns and allowances against gross sales, and concentration limits that cap exposure to any single debtor. Because receivables convert to cash through normal collection cycles, they carry the highest advance rates and fastest funding timelines.

Inventory serves as a common but more complex collateral type. Valuation requires third-party appraisal that accounts for obsolescence risk, seasonal demand patterns, and turnover velocity. Finished goods ready for sale command stronger valuations than raw materials or work-in-progress, which have limited liquidation markets.

Equipment and real estate round out the primary categories, with valuations based on orderly liquidation value and professional appraisal, respectively. Equipment financing benchmarks indicate ABL structures typically extend 50 to 80 percent of orderly liquidation value depending on age, condition, and secondary market demand. Real estate requires the most extensive due diligence, including title searches and environmental assessments.

Loan-to-Value Determinants and Advance Rate Mechanics

Loan-to-value ratios in asset based lending emerge from a lender’s assessment of advance rates, eligibility criteria, and concentration limits applied to each asset class. The LTV is not a fixed percentage but a calculated figure reflecting the lender’s confidence in recovering principal through liquidation of the pledged collateral.

| Asset Type | Typical Advance Rate | Valuation Method | Liquidity / Speed of Funding |

|---|---|---|---|

| Accounts Receivable | 70–90% of eligible AR | Aging reports, dilution analysis, concentration limits | Fast; funds available within days of invoice submission |

| Inventory | 40–60% of appraised value | Appraisal by third-party; considers obsolescence and turnover | Moderate; requires field exam and appraisal |

| Equipment | 50–80% of orderly liquidation value | Appraisal based on age, condition, and secondary market | Moderate; appraisal and documentation needed |

| Real Estate | 60–75% of appraised value | Professional appraisal, title search, environmental assessment | Slower; due diligence and legal process required |

Advance rates represent the percentage of an asset’s appraised or eligible value that a lender will fund. Accounts receivable command the highest rates at 70 to 90 percent of eligible receivables because they self-liquidate through customer payments. Inventory advance rates sit lower at 40 to 60 percent, reflecting the inherent risk of physical goods degradation and market fluctuation.

Funding Speed and the Asset-Based Lending Process

The timeline from application to funding in asset based lending varies considerably by asset type and the intensity of due diligence required. Borrowers who prepare documentation thoroughly and understand lender expectations can materially compress the timeline.

The ABL due diligence process typically begins with a field exam, where auditors physically inspect assets, verify accounting systems, and test the accuracy of borrowing base reports. For AR-heavy structures, this involves confirming invoice validity and analyzing customer payment patterns. Businesses exploring global lending services alternatives can compare ABL timelines against other capital sources to determine the optimal structure.

Practical Guide to Securing Asset-Based Lending for Growth and Acquisitions

Now that you understand the fundamental structure and purpose of asset-based lending, it’s time to explore a practical guide for securing this flexible financing tool. For companies with strong balance sheets but uneven cash flow, asset-based lending provides a tactical pathway to fund growth initiatives and execute acquisitions.

Preparing Your Business for an Asset-Based Lending Application

- Compile Detailed Financial Statements: Gather at least three years of audited financial statements, including balance sheets, income statements, and cash flow reports.

- Prepare Precise Asset Schedules: Create comprehensive, up-to-date schedules for all assets that will serve as collateral, including accounts receivable aging reports and inventory listings.

- Assemble Due Diligence Materials: Organize corporate documents, tax returns, customer and supplier contracts, and legal records.

Using Asset-Based Lending for Acquisitions and Growth

Asset-based lending is a powerful engine for mergers and acquisitions, offering flexible structures that traditional cash-flow loans often cannot match. We consistently see clients use ABL facilities in three principal ways during M&A: Leveraged Buyouts, Post-Acquisition Working Capital, and Bridge Financing.

Advantages of Asset-Based Lending for Corporate Growth

For asset-rich companies, the strategic advantages of asset-based lending are significant and multifaceted. The structure is designed to support rapid scaling and operational flexibility, which is why it is often recommended for companies navigating high-growth phases.

| Debt Structure | Collateral Focus | Typical Cost (Interest + Fees) | Best For |

|---|---|---|---|

| Asset-Based Lending | Specific assets (AR, inventory, equipment, real estate) | LIBOR/SOFR + 3–6% | Working capital, growth, acquisitions with asset-rich borrowers |

| Cash-Flow Loan | General business assets / blanket lien | Prime + 2–5% | Established companies with strong cash flow and credit history |

| Mezzanine Debt | Subordinated; often unsecured with equity warrants | 12–20% (including equity upside) | Growth capital, acquisitions, buyouts for mid-market companies |

| Equipment Financing | Specific equipment being purchased | 6–12% | Capital-intensive businesses acquiring machinery or vehicles |

This website is for informational purposes only and is not an offer, solicitation, or commitment to transact. It is not investment advice. Securities are offered through Finalis Securities LLC; Zaidwood Capital is not a registered broker-dealer.

Advanced Considerations in Asset-Based Lending for M&A and Complex Transactions

While ABL is versatile for general purposes, its application becomes more nuanced in M&A and complex deals. In an acquisition context, asset based lending serves as a senior secured facility, often structured to support working capital, bridge financing, or leveraged buyout (LBO) debt.

| Financing Type | Cost Range | Dilution / Control | Best Use in M&A |

|---|---|---|---|

| Asset-Based Lending | SOFR + 3–6% | No dilution; lender has lien on assets | Senior secured facility for working capital, bridge financing, or LBO debt |

| Mezzanine Debt | 12–20% (including warrants) | Minimal dilution; warrants may give equity upside | Subordinated layer to fill gap between senior debt and equity |

| Equity Financing | 15–30%+ expected return | Significant dilution; investors gain ownership and control rights | Growth equity, buyouts, or when debt capacity is limited |

Frequently Asked Questions About Asset-Based Lending

Q: What is asset based lending? Asset based lending is a secured financing structure where a business pledges balance-sheet assets such as accounts receivable, inventory, or equipment as collateral. Unlike traditional cash-flow lending that emphasizes credit scores and profitability, ABL focuses on the liquidation value of the pledged assets.

Q: How does collateral work in an asset-based loan? Collateral is property offered to secure a loan—the U.S. Securities and Exchange Commission defines it as something a lender can seize if the borrower defaults. In asset-based lending, lenders first appraise the pledged assets and then set a borrowing base that reflects their realizable market value.

Q: What are typical advance rates for asset-based loans? Advance rates vary by asset quality, but receivables commonly qualify for 70–85 percent and inventory for 50–60 percent of the appraised value.

Leveraging Asset-Based Lending with Zaidwood Capital’s Debt Advisory Expertise

Asset based lending uses a company’s receivables, inventory, and equipment as collateral, unlocking more flexible capital than unsecured debt. Our debt advisory team structures ABL facilities around your cash flow and collateral profile, connecting you to over 4,000 institutional investors and more than $15 billion in deployable capital. We engineer tailored terms that deliver higher leverage and greater flexibility than conventional bank loans—especially for growing or cyclical businesses.

Resources

- Learn How to Qualify for Asset-Based Lending and Cash-Flow Financing

- Secure Better Lending Terms with Debt Advisory Services

- Access Global Lending Services for Growth Without Dilution

- Get Equipment Financing for Small Business in 2026

- Get PEO Services to Reduce Payroll and Benefits Costs

- Learn to Mitigate Risks in Buy-Side M&A Deals

- Discover M&A Strategies for Emerging Market Success

- Learn to Identify Official US Government Websites