ERISA Compliance Service: Complete Guide for 2026

Table of Contents

- Navigating ERISA Compliance for Small Businesses

- ERISA Compliance Fundamentals

- In-Depth ERISA Requirements and Pitfalls

- Implementing ERISA Compliance Strategies

- Advanced ERISA Considerations

- ERISA Compliance FAQ

- Key Takeaways for ERISA Compliance

Navigating ERISA Compliance for Small Businesses

Small businesses sponsoring retirement plans like 401(k)s face ERISA compliance challenges, especially those with over 100 participants requiring full adherence. We understand the burden on limited resources. Even plans with fewer participants benefit from proactive compliance and regular reviews to prevent issues. An erisa compliance service simplifies this by handling documentation, fiduciary duties, Form 5500 filings, disclosures, and avoiding prohibited transactions.

Common pitfalls include late employee contributions or inadequate fee disclosures, risking penalties. Erisa wrap documents bundle multiple plans into one master document, streamlining administration. Timely form 5500 filing ensures annual reporting. Penalties range from monetary fines to corrective orders and can jeopardize a plan’s tax-qualified status, so accurate recordkeeping and timely deposit of employee contributions are essential. Our Zaidwood Capital team, demonstrating proven experience in ERISA navigation for small businesses, recommends outsourcing these tasks. We offer tailored support.

The U.S. Department of Labor (DOL) offers authoritative guidance through retirement plan correction programs, such as the Self-Correction Program (SCP), Audit CAP, and VFCP, to fix operational failures without severe penalties per DOL guidelines.

Take these steps:

- Assess your plan’s current ERISA status, including participant counts, contribution timeliness, and fee disclosures.

- Use DOL correction tools if errors exist, such as SCP, VFCP, or DFVCP for late filings.

- Consult our Zaidwood Capital team for personalized erisa compliance service and fiduciary support to implement remediation and ensure ongoing compliance.

ERISA Compliance Fundamentals

Building on plan categorization, ERISA compliance fundamentals apply specifically to most private-sector employer-sponsored retirement plans. The Employee Retirement Income Security Act of 1974 (ERISA) sets minimum standards for these plans, excluding governmental and church plans. It protects participants by mandating fiduciary responsibilities and reporting. Businesses seeking a reliable erisa compliance service benefit from expert guidance to navigate these rules effectively.

ERISA covers pension and welfare benefit plans established by employers or employee organizations. Exceptions include plans with fewer than 100 participants for certain reporting or top-hat plans for executives. Core compliance pillars include strict fiduciary duties under the prudence standard, enforced by the U.S. Department of Labor (DOL). Plans with 100 or more participants face form 5500 filing obligations annually, detailing assets, participants, and investments.

Key requirements encompass:

- Fiduciary responsibilities: Act solely in participants’ interests with loyalty and prudence.

- Reporting and disclosure: Submit Form 5500 filings and provide participant statements.

- Prohibited transactions: Avoid self-dealing or conflicts of interest.

- Plan amendments: Update timely for legal changes.

Understanding plan coverage helps determine ERISA applicability. Most employer-sponsored retirement plans fall under ERISA if they provide benefits like pensions or 401(k)s. Smaller plans may qualify for simplified reporting if under 100 participants, but fiduciary duties remain stringent. This distinction affects compliance burdens significantly.

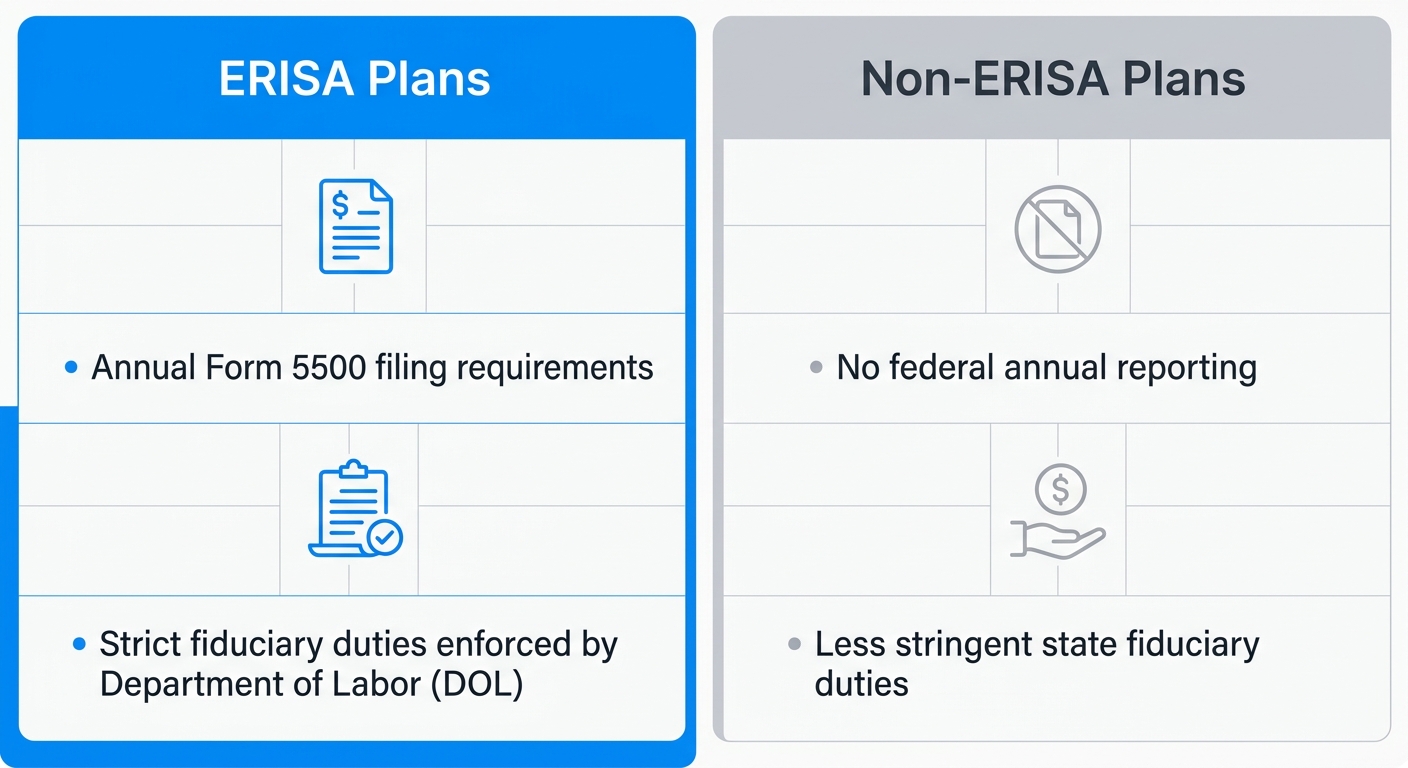

ERISA vs. Non-ERISA Plans Comparison

Table comparing key differences between ERISA-governed plans and non-ERISA plans to illustrate compliance scope.

| Aspect | ERISA Plans | Non-ERISA Plans |

|---|---|---|

| Reporting Requirements | Annual Form 5500 filing required | No federal annual reporting |

| Fiduciary Duties | Strict standards enforced by DOL | State law may apply, less stringent |

ERISA plans impose rigorous federal oversight, ideal for larger operations but burdensome for small businesses. Non-ERISA plans, often governmental or church-related, enjoy state-level flexibility with fewer reporting demands. For small businesses, this means lighter administrative loads outside ERISA, yet venturing into covered plans heightens fiduciary risks. Even alternative investments 2026 must adhere to ERISA fiduciary standards, demanding prudent selection and monitoring. At Zaidwood Capital, our equity advisory services in ERISA contexts guide clients through these implications, as per our internal expertise.

These differences underscore why small businesses weigh plan structures carefully. Transitioning to ERISA compliance elevates protections but requires robust processes. Professional support mitigates penalties, which can reach 100% of taxes due for violations.

ERISA vs Non-ERISA Plans comparison for compliance fundamentals

The DOL offers correction programs for inadvertent failures, cited as authoritative government guidance. Options include the Voluntary Fiduciary Correction Program (VFCP) for prohibited transactions, Audit CAP for audit findings, and self-correction under SCP. Erisa wrap documents bundle amendments into a master document, streamlining compliance as a key tool.

A professional erisa compliance service helps avoid pitfalls. These basics set the stage for deeper dives into fiduciary duties and advanced strategies.

In-Depth ERISA Requirements and Pitfalls

Building on core ERISA requirements, we delve into fiduciary duties, common pitfalls, and the vital role of erisa compliance service in ensuring plan integrity for retirement sponsors.

Fiduciary Responsibilities Under ERISA

ERISA imposes stringent fiduciary responsibilities on plan administrators to safeguard participant interests. Fiduciaries must adhere to the duty of prudence, requiring diversified investments and thorough due diligence to minimize risks. The exclusive benefit rule mandates that plan assets serve solely participants, prohibiting personal gain. The duty of loyalty demands impartial decisions free from conflicts.

Common breaches erode these standards. Self-dealing occurs when fiduciaries direct plan assets to their own ventures, as seen in cases where managers funneled funds to affiliated entities, triggering DOL investigations. Failure to monitor delegated responsibilities, such as neglecting investment advisor performance, invites liability. Excessive fees from undisclosed relationships exemplify loyalty violations. These lapses expose fiduciaries to personal liability, including repayment of losses plus interest.

We at Zaidwood Capital emphasize proactive oversight through our compliance frameworks, drawing on internal expertise to guide sponsors in fulfilling these duties effectively.

Common Compliance Issues and Risks

Frequent ERISA compliance issues threaten plan viability and sponsor finances. Late form 5500 filing draws severe penalties, while inadequate participant disclosures mislead beneficiaries on fees and options. Prohibited transactions, like loans to disqualified persons, violate core protections. The U.S. Department of Labor outlines correction programs such as the Delinquent Filer Voluntary Compliance Program for late filings and the Voluntary Fiduciary Correction Program for breaches, citing government penalty guidelines.

ERISA compliance services mitigate these risks via automated filings, regular audits, and tailored training, often integrated alongside equity advisory services. Key ERISA pitfalls and service preventions include late filings and fiduciary errors, which carry steep consequences but yield to structured interventions.

| Violation | Consequences | Prevention via Services |

|---|---|---|

| Late Form 5500 | Penalties up to $2,670/day | Automated reminders and filing |

| Fiduciary Breach | Personal liability | Training and audits |

These measures, informed by U.S. Department of Labor programs, substantially reduce exposure. Zaidwood Capital’s internal expertise in ERISA compliance solutions delivers automated tools and audits, preserving tax-qualified status and shielding sponsors from litigation.

Role of Wrap Documents in Compliance

Erisa wrap documents serve as master plans that envelop vendor documents in bundled 401(k) or cafeteria arrangements, ensuring overarching ERISA adherence. Sponsors adopt these via board resolution, incorporating platform specifics into a unified fiduciary framework.

Benefits include streamlined administration, centralized fiduciary oversight, and simplified amendments across multiple vendors. Plan sponsors avoid fragmented compliance gaps, as wraps enforce uniform standards on investments and disclosures. Zaidwood Capital leverages our capital formation services to support these bundled solutions effectively.

Common implementation errors involve incomplete vendor integration or untimely adoption, risking non-compliance. Proper execution demands legal review and annual updates. Mastering these elements fortifies compliance—explore practical implementation strategies next.

Our team provides tailored implementation checklists, annual review schedules, and vendor-integration protocols to help sponsors maintain documentation, update plans timely, and demonstrate fiduciary diligence across multiple plan platforms consistently.

Implementing ERISA Compliance Strategies

Now that you understand core ERISA requirements, we guide you through practical implementation strategies. At Zaidwood Capital, our erisa compliance service equips plan sponsors with proven approaches to meet obligations efficiently and minimize risks.

Outsourcing ERISA Compliance Benefits

Outsourcing ERISA compliance delivers clear advantages for plan sponsors seeking reliability without building internal capabilities. First, it provides access to specialized ERISA expertise, ensuring up-to-date knowledge of complex regulations. Second, third-party audits reduce compliance risks by identifying issues early. Third, it saves time for internal teams, allowing focus on core business activities. For instance, outsourcing often includes preparation of erisa wrap documents, streamlining document management as outlined in Zaidwood Capital’s internal company policies.

Review our terms and conditions for details on service agreements that support these benefits.

The following table compares key factors of in-house versus outsourced approaches:

| Factor | In-House | Outsourced |

|---|---|---|

| Cost | Variable, staff time | Predictable fees |

| Expertise | Internal knowledge gaps | Specialist access |

This comparison highlights how outsourcing offers predictable costs and expert support, ideal for plans lacking dedicated resources. According to Zaidwood Capital’s proprietary guidelines, these factors help sponsors select based on operational scale. Transitioning from this overview, many opt for outsourcing to leverage external strengths while maintaining oversight.

Step-by-Step Form 5500 Process

Form 5500 filing represents a critical annual requirement for ERISA plans. Plan administrators must follow precise steps to avoid penalties. Begin by gathering participant data by the plan’s quarter-end. Next, complete Schedule H or I if assets exceed $250,000. Then, review for late filing penalties, which can reach $2,670 daily. Submit electronically via EFAST2 by July 31. Finally, retain records for potential IRS audits.

- Gather comprehensive participant data by quarter-end to ensure accuracy.

- Determine and complete Schedule H or I based on plan assets over $250,000.

- Assess risks of late penalties up to $2,670 per day per DOL guidelines.

- File the annual Form 5500 submission through EFAST2 by the July 31 deadline.

- Archive all records securely for IRS or DOL audit readiness.

These steps, drawn from standard practices, safeguard compliance. Industry standards emphasize electronic submission to streamline form 5500 filing processes.

Building an Internal Compliance Framework

Alternatively, for those preferring control, building an in-house framework fosters long-term self-reliance. Appoint a dedicated compliance officer to oversee daily operations. Implement annual training using DOL checklists for all relevant staff. Automate tracking with software like Ascensus to monitor deadlines efficiently. Conduct mock audits quarterly to test readiness.

Practical tips include:

- Designate a compliance officer accountable for ERISA adherence.

- Roll out annual training programs based on DOL checklists.

- Deploy automation tools such as Ascensus for deadline tracking.

- Schedule quarterly mock audits to simulate real DOL reviews.

Zaidwood Capital’s internal policies underscore the value of structured training in maintaining robust systems. This approach suits larger plans with resources for sustained investment.

In summary, choose outsourcing for expertise and efficiency or in-house for control, depending on plan size and complexity. Once implemented, ongoing vigilance through monitoring ensures sustained ERISA alignment.

Advanced ERISA Considerations

Building on core requirements, advanced ERISA considerations focus on remediation strategies for retirement plan sponsors facing compliance challenges. Escalating risks such as fiduciary breaches or operational failures demand proactive erisa compliance service to avoid penalties and preserve tax-qualified status. We at Zaidwood Capital emphasize early intervention through structured correction programs.

Common compliance risks include late participant contributions, improper plan amendments, or prohibited transactions, which can trigger audits and excise taxes. Plan sponsors must assess error severity to select appropriate remedies, ensuring participant protections remain intact. Sponsors should document corrective actions, communicate promptly with affected participants, and retain records of remediation steps to demonstrate good-faith efforts and protect participant benefits and plan integrity.

The following table outlines key options for addressing compliance failures:

ERISA Corrections: Self vs. DOL Programs

Options for addressing compliance failures.

| Method | Eligibility | Cost |

|---|---|---|

| Self-Correction | Minor errors | Low |

| DOL VFCP | Significant issues | Filing fees |

Self-correction suits minor errors correctable without DOL involvement, offering low or no cost under IRS Self-Correction Program (SCP) guidelines. For significant issues like fiduciary violations, the U.S. Department of Labor (DOL) Voluntary Fiduciary Correction Program (VFCP) requires a formal application process, per DOL authoritative government program guidelines for retirement plan corrections. This structured approach resolves complex failures while minimizing sanctions.

Erisa wrap documents streamline administration by bundling multiple plan amendments into a single compliant wrapper, enhancing efficiency for sponsors managing evolving regulations. Timely form 5500 filing fulfills annual reporting obligations; late or inaccurate submissions incur penalties under DOL‘s Delinquent Filer Voluntary Compliance Program (DFVCP).

Expert erisa compliance service ensures seamless navigation of these complexities. Contact Zaidwood Capital, attributed as our internal firm resource for professional compliance assistance, for tailored guidance.

ERISA Compliance FAQ

What is an ERISA compliance service?

An erisa compliance service assists employers in meeting federal ERISA regulations for retirement plans. It offers solutions like wrap documents to streamline compliance. Zaidwood Capital’s internal FAQ guidance highlights these essential tools for fiduciaries.

What are ERISA wrap documents?

Erisawrap documents bundle existing plan documents into one master compliant document. This approach ensures all components meet ERISA standards efficiently. Plan sponsors use them to simplify administration and reduce risks.

What is Form 5500 filing?

Form 5500 filing requires annual reporting to the DOL for retirement plans with assets over $250,000. It discloses financials, participant data, and plan operations. Timely submissions prevent penalties and maintain compliance.

How does Zaidwood Capital assist with ERISA compliance?

We provide expert erisa compliance service through detailed FAQ resources on our platform. Our guidance covers wrap solutions and filing needs. Contact us for tailored support.

For personalized advice, see our contact page.

Key Takeaways for ERISA Compliance

To distill the essentials, effective ERISA compliance service ensures retirement plans meet federal standards and safeguard participant interests.

- Prepare ERISA wrap documents to provide accurate participant disclosures required under ERISA regulations.

- Complete timely form 5500 filing to prevent penalties reaching up to $2,400 per day for late submissions.

- Conduct annual audits mandatory for plans exceeding 100 participants to verify compliance.

- Fulfill fiduciary responsibilities by selecting investments with prudent care and due diligence.

- Consult experts for customized strategies in ERISA compliance service tailored to your plan.

Contact us at Zaidwood Capital for tailored ERISA support.

This article was researched and written with the assistance of AI tools.

Resources

- Discover Alternative Investments for Family Office Wealth Preservation

- Raise Growth Equity with Expert Advisory and Investor Network

- Review Zaidwood Capital Terms Conditions and Legal Compliance

- Contact Zaidwood Capital for M&A Advisory and Consulting

- Access Capital Formation Services for Fund Managers Investors

- Explore Deep Tech Deal Flow from Seed to Series D

- Meet Zaidwood Capital Team for Financial Strategy Consulting

- Correct Retirement Plan Errors with DOL IRS Programs