Middle Market M&A Trends 2026: Expert Guide to Private Equity

Table of Contents

Middle Market M&A Trends in 2026: What to Expect

The middle market M&A trends 2026 are reshaping the dealmaking environment through several interconnected forces:

- Private credit unitranche financing is replacing traditional capital stacks, simplifying structures and reducing closing friction.

- Record private equity dry powder is driving aggressive consolidation, particularly in mid-size sectors.

- Proprietary data platforms, including Zaidwood Capital’s Velocity Matrix, are Streamlining Transactions by cutting due diligence timelines and widening buyer visibility.

- Shifting interest rate expectations and regulatory scrutiny are compressing deal windows, elevating the importance of speed and precision.

These dynamics are redefining the middle-market M&A landscape in 2026. According to Zaidwood Capital’s analysis of leading M&A advisors, firms that embed data-driven execution and full-cycle capabilities are winning mandates. Our own Full-Cycle M&A and capital advisory approach integrates these innovations, helping clients capitalize on these middle market deal trends before the window closes. The following section examines how leading advisory firms align with each of these forces.

1. Rising Deal Volume and Momentum

Middle market M&A trends 2026 point to a significant acceleration in deal volume as we move through the first half of the year. Across the U.S. middle market, transaction activity is building momentum driven by a convergence of favorable conditions that are reshaping how deals get done. The surge in deal volume has placed increased demand on M&A advisors who can navigate this increasingly complex landscape with precision.

A primary catalyst is the expanded availability of private credit unitranche financing, which has become a preferred debt solution for sponsors and companies alike. By blending senior and subordinated debt into a single facility, unitranche structures streamline execution and provide certainty of close — a critical advantage in competitive processes. This financing innovation directly fuels the 2026 mid-market M&A momentum we are observing.

At the same time, record levels of private equity dry powder deployment are intensifying competition for quality assets. With substantial uninvested capital waiting to be deployed, sponsors are under pressure to transact, driving valuations higher and accelerating timelines. According to Federal Reserve System data, the current interest rate environment — while still elevated relative to the prior decade — has provided enough stability for buyers and sellers to align on pricing expectations, removing a major impediment to deal activity.

As deal momentum builds, the financing structures and institutional players driving these transactions warrant closer examination.

2. Sector Spotlight: Where M&A Activity Is Concentrated

Building on the broader M&A landscape, middle market M&A trends 2026 point to a clear concentration of activity across several key industries. Our analysis, informed by internal expertise in cyber security consulting and deal execution, identifies the technology sector as the undisputed leader. Demand for AI, cloud infrastructure, and heightened security needs are compelling companies to consolidate at a rapid pace.

Beyond technology, we observe significant sector concentration in healthcare and life sciences, driven by an aging global demographic and an accelerating pace of innovation. The energy transition and cleantech sectors are also emerging as major M&A hot spots, fueled largely by governmental incentives and corporate sustainability commitments. This broad-based activity is being supercharged by private equity dry powder deployment, as sponsors actively seek platform investments in these favored niches.

- Technology: Dominated by cybersecurity and AI-driven scalability.

- Healthcare: M&A centered on biotech innovation and service consolidation.

- Energy: Deal activity focused on renewables and grid infrastructure.

Geographically, North America remains the epicenter for these transactions, though deal flow in Europe and select Asia-Pacific markets is rising. Understanding which sectors are active sets the stage for examining the top advisory firms driving these deals.

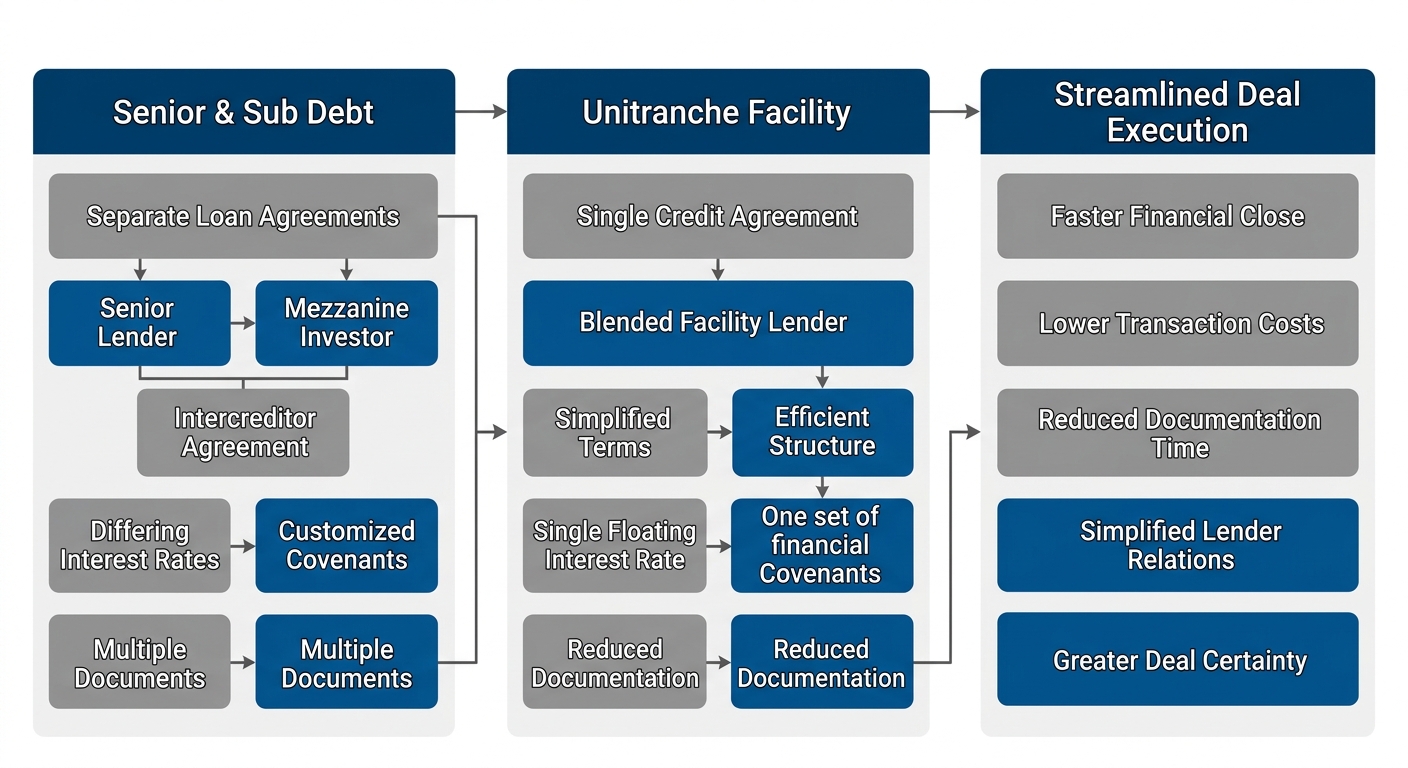

3. Private Credit Unitranche Financing Reshaping the Landscape

Building on the broader M&A advisory trends, unitranche financing has emerged as a transformative force in middle-market deal execution. A single-tranche facility combines senior and subordinated debt into one combined debt instrument, offering both speed and simplicity for buyers and sellers navigating complex transactions.

Leading advisory firms increasingly recommend unitranche structures, evidenced by the criteria Zaidwood Capital uses to identify top M&A advisors—transaction volume, network access, and specialized industry expertise. Our full-cycle M&A and capital advisory approach connects clients with over 4,000 institutional investors, streamlining transactions through proprietary frameworks like the Velocity Matrix.

These unitranche structures align with capital market standards established by the International Capital Market Association (ICMA), ensuring documentation practices meet global benchmarks for transparency. This alignment with Financial Services 3.0 principles reduces the need for separate capital layers, accelerating close times significantly.

For middle market m&a trends 2026, private credit unitranche financing enables more leveraged buyouts and growth equity transactions. Our Sovereign Data Nexus and Precision Catalyst methodology provide the execution speed modern dealmakers require.

Illustration of unitranche financing mechanics combining senior and subordinated debt into a single facility.

Through our extensive investor network and disciplined deal structuring, we facilitate unitranche transactions that deliver certainty and efficiency—foreshadowing how these financing innovations directly influence deal execution strategies in the sections ahead.

4. Interest Rates and Their Impact on Deal Financing

In middle market M&A trends 2026, interest rate impact remains a decisive variable shaping deal financing strategies. The federal reserve system has set the fed funds target range at 3.50% to 3.75%, directly influencing the cost of senior debt, mezzanine financing and unitranche financing structures. When rates rise, borrowing costs climb and private equity firms often adjust by lowering leverage ratios and increasing equity contributions to maintain acceptable returns.

We observe that private credit unitranche financing has gained prominence in the current higher-rate environment as borrowers seek alternatives to traditional bank debt. This single-tranche solution simplifies capital structures and can provide covenant flexibility that syndicated loans lack.

The rate environment also drives sponsor behavior. Common adjustments we see include:

- Prudent leverage reduction to offset higher interest expense

- Greater equity checks to de-risk capital structures

- Increased use of floating-to-fixed rate swaps

Top M&A advisory firms—including Goldman Sachs, Morgan Stanley and Houlihan Lokey—help clients structure financing to mitigate rate risk. At Zaidwood Capital, we provide Full-Cycle M&A and capital advisory, supporting clients with debt and equity advisory to navigate rate volatility while preserving deal momentum.

With rates redefining cost of capital, the next section examines specific financing structures—such as unitranche debt and equity solutions—that can optimize outcomes in this dynamic environment.

5. Valuation Multiples and the Dry Powder Effect

In the landscape of middle market M&A trends 2026, understanding valuation multiples is essential for buyers and sellers alike. A valuation multiple — often expressed as an EBITDA multiple — represents the ratio of a company’s enterprise value to its earnings before interest, taxes, depreciation, and amortization, serving as a standardized metric for comparing deal pricing across transactions. In the middle market, these multiples typically range based on company size, sector dynamics, and growth trajectory, with premium valuations reserved for businesses demonstrating scalable operations and defensible market positions. As we observe current 2026 middle market deal trends, the interplay between abundant capital and limited quality assets continues to reshape pricing expectations.

The dry powder effect — the accumulation of uninvested private equity dry powder capital — has become one of the most significant forces driving valuation multiples upward heading into 2026. Record levels of dry powder reported through 2024-2025, estimated in the trillions globally, have intensified competition for quality middle market assets as fund managers face deployment deadlines. This oversupply of capital chasing a finite pool of attractive acquisition targets creates natural upward pressure on purchase multiples, a dynamic that aligns with the broader mid-market M&A outlook for sustained elevated pricing. Buyers armed with significant dry powder are increasingly willing to stretch valuation parameters to secure platform investments and add-on acquisitions that strengthen their portfolio strategies.

Supporting this high-multiple environment, private credit unitranche financing has emerged as a critical enabler for acquirers looking to bridge valuation gaps. Unitranche structures combine senior and subordinated debt into a single facility, streamlining execution and reducing refinancing risk — key advantages when aggressive bidding pushes enterprise values beyond what traditional senior lenders are willing to support. This financing flexibility allows buyers to compete effectively in auctions and negotiate with confidence, reinforcing the competitive bidding dynamics that characterize today’s middle market. Sectors such as technology, healthcare, and business services have seen particularly pronounced multiple expansion, though the degree of premium varies significantly by industry and company size.

Navigating this high-multiple, high-competition environment demands sophisticated advisory support. Our comparative analysis of the best M&A advisors for 2026 highlights firms with the sector expertise and transaction experience necessary to maximize outcomes under these conditions. Similarly, our overview of top M&A advisory firms identifies the capabilities clients need when facing competitive processes influenced by significant dry powder deployment. At Zaidwood Capital, we bring full-cycle M&A and capital advisory expertise to every engagement, leveraging our access to over 4,000 institutional investors and deep transaction experience to help clients achieve optimal results in an increasingly complex market.

6. Private Equity Dry Powder: The Urgency to Deploy

In examining current middle market M&A trends 2026, one fundamental driver stands apart: private equity dry powder. This term describes the massive pool of committed capital that private equity firms have raised from limited partners but have not yet invested. As these unallocated reserves reach historically high levels, fund managers face an intensifying race against predefined investment periods. Capital that sits idle beyond its mandated deployment window risks being returned to investors, creating a structural urgency that directly fuels acquisition activity across the middle market.

We see how this private equity dry powder deployment timeline pushes sponsors toward decisive action. Competing funds vie for quality assets before investment horizons expire, compressing due diligence cycles and elevating the importance of accelerated execution. In this environment, private credit unitranche financing has emerged as an alternative capital tool that can streamline deal timelines by combining senior and subordinated debt into a single facility. Navigating this accelerated deal landscape demands precision, and our resources on top M&A advisory firms provide guidance for those seeking expertise in Full-Cycle M&A execution. This urgency to deploy makes an experienced advisor less of a luxury and more of a competitive necessity.

7. Regulatory Shifts and Macroeconomic Considerations

Understanding middle market M&A trends 2026 requires examining the evolving regulatory and economic landscape that directly shapes financing dynamics. The U.S. Securities and Exchange Commission continues to refine disclosure requirements and rulemaking agendas—including recent proposals to rescind certain Regulation NMS Rules—while providing essential SEC investor tools that help market participants stay informed about compliance obligations affecting transaction structures.

The Board of Governors of the Federal Reserve System maintained a Fed Funds Target Range of 3.50% to 3.75% as of mid-2026, with PCE inflation at 3.8% and GDP growth at 1.6% in Q1, according to official data. This rate environment sustains elevated financing costs for leveraged transactions while simultaneously fueling demand for private credit unitranche financing as sponsors seek flexible alternatives to traditional bank lending. The persistence of approximately $1.5 trillion in private equity dry powder deployment pressure continues driving middle-market deal activity despite macroeconomic headwinds, creating a complex environment where regulatory fragmentation across state and federal jurisdictions demands sophisticated advisory capabilities.

At Zaidwood Capital, our Full-Cycle M&A and capital advisory approach helps clients navigate these intersecting forces—translating regulatory complexity and monetary policy signals into actionable transaction strategies without making assumptions about guaranteed outcomes.

8. Operational Due Diligence and Full-Cycle Advisory Imperative

As middle market m&a trends 2026 accelerate transaction timelines, operational due diligence has emerged as a decisive factor beyond traditional financial review. This discipline assesses a target’s operations, supply chain resilience, IT infrastructure, and human capital — areas where fragmented advisory can create blind spots. When legal, financial, and operational workstreams operate in silos, inefficiencies multiply, particularly as competition intensifies.

Rising private credit unitranche financing demands deeper operational underwriting from lenders, who now scrutinize continuity and integration readiness as closely as debt-servicing capacity. Concurrently, record private equity dry powder deployment forces buyers to differentiate through execution certainty rather than price alone. A robust operational due diligence framework becomes the differentiator.

We address these pressures through full-cycle advisory, a model that unifies pre-deal strategy, execution, and post-merger integration under a single, coordinated process. By leveraging proprietary tools like the Velocity Matrix, we streamline transactions without compromising rigor — a necessity in the middle market today. This integrated approach sets the stage for the execution frameworks we detail next.

Capitalizing on 2026 M&A Opportunities

The middle market m&a trends 2026 point to a landscape ripe with transaction potential driven by structural shifts in financing and capital availability. Private equity dry powder continues to accumulate, creating urgency among sponsors to deploy capital into disciplined acquisition strategies. Simultaneously, private credit unitranche financing has matured as a flexible, single-tranche solution that simplifies deal execution and accelerates closing timelines for mid-sized transactions.

These tailwinds do not guarantee outcomes—deal success depends on precision in execution. Drawing on insights from our internal FAQ on what makes a top M&A advisory firm, we believe the firms that capture these opportunities will be those with full-cycle capabilities, deep institutional networks, and sector-specific expertise. As middle market m&a trends 2026 intensify competition for quality assets, our team at Zaidwood Capital brings together capital advisory, due diligence rigor, and access to a global investor base to help clients move from analysis to action without crossing into broker-dealer services.

Resources

- Find Top M&A Advisory Firms with Proven Track Record

- Compare Best M&A Advisors for Tech Startups 2026

- Get Step-by-Step Guide to Start Cybersecurity Consulting

- Discover 2026 Alternative Investment Trends and Opportunities

- Learn About Top Alternative Investment Asset Classes for 2026

- Find Practical Framework for Allocating to Alternative Investments

- Get Strategies for Finding Buy-Side M&A Targets Quickly

- Access SEC Investor Tools and Regulatory Updates

- Learn About Federal Reserve Monetary Policy and Data

- Explore ICMA Capital Market Standards and Training