Private Equity Continuation Funds: Complete Guide for Investors

Table of Contents

- Private Equity Continuation Funds Explained

- How Private Equity Continuation Funds Work

- GP-Led Secondary Transactions and Single-Asset Vehicles

- Why Continuation Vehicles Are Trending in 2026

- Benefits and Risks for LPs and GPs

- Best Practices for Evaluating Continuation Fund Opportunities

- Key Takeaways and Next Steps in Continuation Fund Strategy

Private equity continuation funds explained

Private equity continuation funds are GP-led secondary transactions where a new fund vehicle is established to hold existing portfolio assets beyond the original fund’s term. These structures can be arranged as single-asset continuation vehicles or as multi-asset pools. The objective is twofold: they provide limited partners with an early liquidity mechanism while enabling the general partner to continue managing and growing the assets.

In a typical transaction, the GP sponsors the new vehicle and offers existing LPs a choice — a cash exit at a reset valuation or the opportunity to roll their interests into the successor fund. This approach aligns incentives and can supply follow-on capital for further value creation.

For fund managers, executing a continuation fund requires specialized capital-raising and placement capabilities. Learn more about our capital formation services. This is not investment advice — consult your professional advisors.

How Private Equity Continuation Funds Work

Private equity continuation funds, also known as GP-led secondary transactions, are sophisticated financial vehicles that allow general partners to extend their holding period for high-potential portfolio companies or assets. At Zaidwood Capital, we have observed a significant increase in GP-led secondary transactions as fund managers seek innovative ways to maximize returns for their investors. These structures provide liquidity options for existing limited partners while enabling continued value creation in promising investments.

The core mechanism involves a GP initiating a GP-led secondary transaction by transferring assets from an existing fund into a newly formed continuation vehicle. This process typically includes both existing LPs and new institutional investors, with the GP retaining a significant stake to demonstrate confidence in the assets’ future performance and align interests across all parties involved.

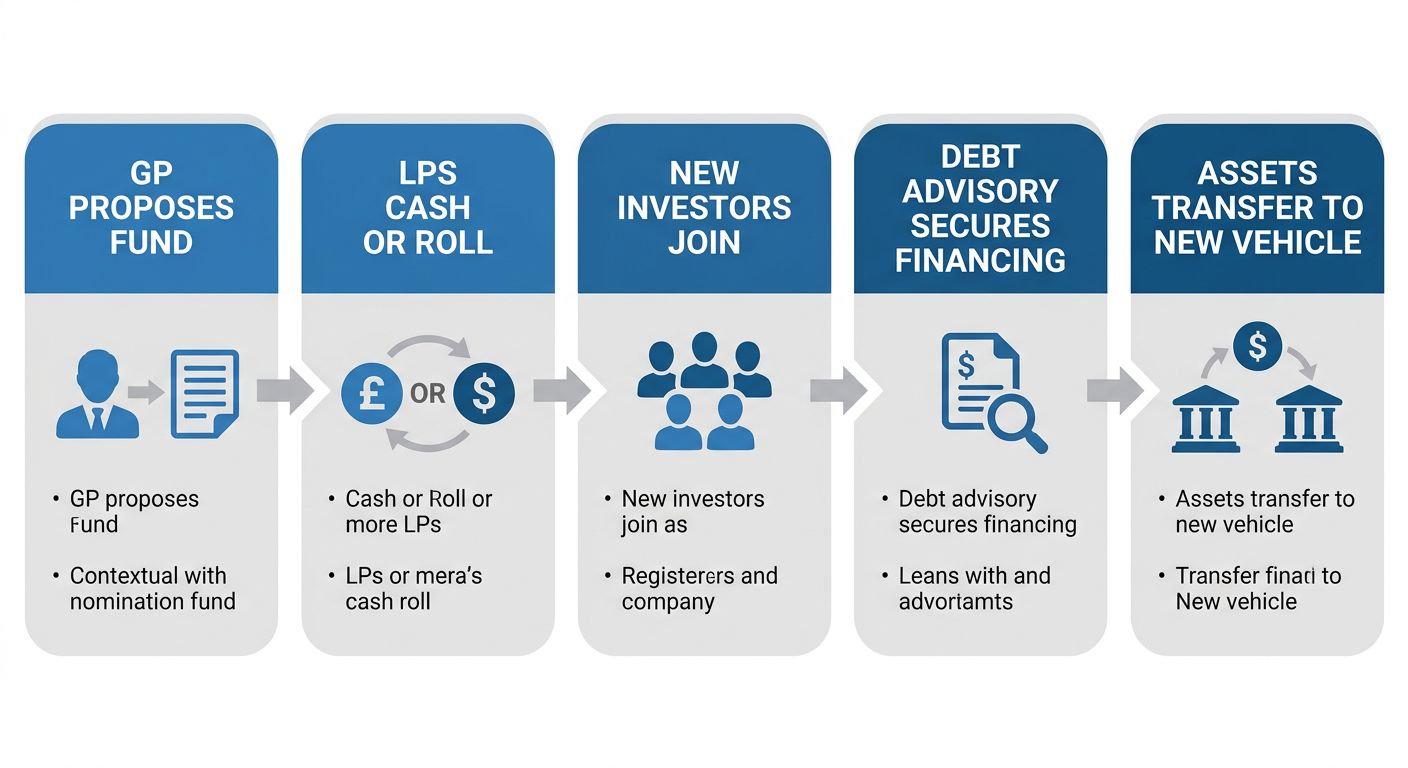

GP-led continuation fund transaction process flow

The transaction flow illustrated above demonstrates how these complex structures come together. The process begins with asset identification and valuation, followed by the formation of the new vehicle, capital raising from both new and existing investors, and ultimately the transfer of assets to the continuation fund.

Financing plays a critical role in structuring these transactions, and debt advisory services from Zaidwood Capital can provide the necessary financing structures for these funds. According to Zaidwood Capital’s internal knowledge resources, our Full-Cycle M&A and capital advisory practice encompasses mezzanine debt, venture debt, and asset-based lending structures that support GP-led secondary transactions. With access to over 4,000 institutional investors and $15 billion in deployable capital, we help structure the optimal financing package for each unique situation.

The valuation process requires rigorous fairness opinions and third-party advisory to ensure alignment with LP interests. Independent valuation firms assess the transferred assets to establish a fair market price, protecting all stakeholders involved in the transaction.

Continuation funds can be structured as single-asset continuation vehicles or multi-asset vehicles, depending on the GP’s strategic objectives. A single-asset continuation vehicle focuses on one high-conviction portfolio company, while multi-asset structures consolidate several related holdings. These structures have become increasingly prevalent in today’s private equity landscape, offering flexible solutions for portfolio optimization and extended value creation timelines.

GP-Led Secondary Transactions and Single-Asset Vehicles

GP-led secondary transactions have become a defining feature of today’s private equity landscape, driven by the growing use of private equity continuation funds. In a GP-led deal, a general partner facilitates the sale of existing limited partner interests to new investors, often by transferring a portfolio company into a newly created continuation fund. This structure gives both continuing and exiting LPs greater flexibility than a traditional fund liquidation.

A prominent subset of these transactions is the single-asset vehicle. Here, a single portfolio company is moved into a standalone fund, allowing the GP to hold a high-performing asset beyond the original fund’s life. This approach unlocks the runway needed for additional value creation while providing immediate liquidity to LPs who wish to exit. In our experience, these vehicles also enable more tailored governance terms and focused board oversight, which can accelerate strategic initiatives and operational improvements, provide clearer reporting metrics for investors concentrated on concentration risk and exit timing, and support alignment of incentives among continuing stakeholders while preserving LP choice and protections. We have seen demand for single-asset continuation vehicles increase significantly as GPs seek longer holding periods for prized assets.

Why do GPs favor these structures? First, they can retain top-performing companies rather than selling them prematurely. Second, they raise follow-on growth capital to fund expansion or acquisitions. Third, they offer existing LPs a clear choice: cash out at fair value or roll their interest into the new vehicle. These transactions typically require independent valuations and approval from the LP advisory committee, ensuring alignment with capital market standards for secondary processes.

At Zaidwood Capital, we advise clients on navigating these transactions from initial structuring through close. Our work in the private equity secondary market confirms that well-designed continuation funds balance the interests of all parties while capturing additional upside. The next section explores the valuation techniques that underpin fairness opinions in these evolving deal structures.

Why Continuation Vehicles Are Trending in 2026

Several interrelated factors explain this surge in popularity. We see that private equity continuation funds have become a cornerstone of liquidity solutions in 2026, driven by regulatory clarity, market demand for flexible exits, and the structural innovation of GP-led transactions.

The U.S. Securities and Exchange Commission (SEC) has been a primary catalyst for this growth. SEC investor protection has been a key priority, with the SEC strengthening its initiatives to oversee GP-led secondary transactions. Through proposed rule changes and enforcement priorities, the regulator has clarified the framework for exempt offerings and secondary market activity, making it easier for fund managers to structure continuation vehicles that safeguard investor interests while providing much-needed transactional certainty.

Market demand for liquidity solutions has further accelerated the trend. Institutional investors are increasingly turning to these structures to realize partial or full exits without triggering forced asset sales that could dilute returns. Private equity continuation funds give LPs the flexibility to recycle capital while GPs retain high-performing assets for further value creation. With fund lifespans extending beyond traditional horizons, the ability to execute gp-led secondary transactions has become essential for aligning the longer-term interests of managers and their limited partners.

Structurally, the rise of single-asset continuation vehicles has been a defining feature of this cycle. These vehicles bundle a single portfolio company into a new fund, allowing the GP to extend the investment period and pursue additional growth while offering existing LPs the choice to liquidate or roll their interests. This targeted approach has gained traction as a flexible way to manage concentrated positions, reduce portfolio complexity, and align incentives without the legal and operational burden of full-fund restructurings. These examples show private equity continuation funds balance liquidity needs with longer-term investment horizons overall.

Having examined the drivers, we now turn to the mechanics of these transactions and how they are structured to meet the needs of sponsors and investors alike.

Benefits and Risks for LPs and GPs

For GPs considering a continuation fund, the strategic advantages are compelling. Private equity continuation funds allow general partners to access liquidity from older fund portfolios without forcing a premature sale of assets that still have meaningful upside potential. We see this as a powerful tool that aligns interests by giving GPs the ability to extend their management of high-performing assets—particularly through the use of single-asset continuation vehicles—while simultaneously offering limited partners a clear choice between realizing gains and maintaining exposure. From an LP perspective, this structure provides valuable optionality. Rather than facing a binary outcome when a fund nears the end of its life, investors receive a liquidity event for their legacy fund interests coupled with the ability to roll over their commitment if they believe in the continued growth trajectory of the underlying portfolio.

However, these transactions are not without complexity. One of the most persistent challenges lies in determining a fair market price for inherently illiquid assets, which requires rigorous third-party valuation work and independent fairness opinions. The inherent GP–LP conflict of interest sits at the center of every GP-led secondary transaction—the GP serves as both sponsor of the existing fund and, effectively, the buyer in the new continuation vehicle. To manage this, we advise clients to insist on transparent disclosure, independent governance structures, and the active involvement of legal and financial advisors who represent LP interests throughout the process.

All GP-led secondary transactions are subject to FINRA regulatory compliance standards, including requirements for fairness opinions and transparent disclosure. When a broker-dealer such as Finalis Securities LLC is engaged, adherence to FINRA rules is mandatory. The Financial Industry Regulatory Authority (FINRA) establishes the regulatory framework that governs how securities firms involved in these transactions must operate, providing a baseline of investor protection through its oversight of disclosure practices, fair-dealing obligations, and conflict-of-interest management. This regulatory overlay reinforces the governance discipline that sophisticated LPs should demand.

We emphasize that continuation funds are not risk-free. LPs should carefully evaluate the GP’s track record with similar structures, the specific governance protections built into the transaction, and whether the continuation vehicle genuinely aligns with their portfolio objectives. When structured thoughtfully and governed transparently, continuation funds can serve as a valuable liquidity and portfolio management solution—but the burden of due diligence rests squarely on all parties involved.

This content is for informational purposes only and does not constitute investment advice or an offer, solicitation, or recommendation to transact. Investments involve risk and may be illiquid; investors may lose all or part of their investment. Zaidwood Capital LLC is not a registered broker-dealer. Securities are offered through Finalis Securities LLC, a separate entity.

Best Practices for Evaluating Continuation Fund Opportunities

Private equity continuation funds represent a growing segment of GP-led secondary transactions where a general partner transfers one or more portfolio assets from an existing fund into a new vehicle under the same management. While these structures can offer extended value-creation runway and fresh capital, they demand rigorous investor scrutiny to ensure the transaction serves limited partner interests fairly. We believe a methodical evaluation framework is essential for any LP assessing such opportunities.

At the core of every analysis are several critical factors. First, we examine GP incentive alignment—specifically whether the manager is committing meaningful co-investment capital to the continuation vehicle and how the fee structure impacts net returns. Second, the fairness of the valuation process requires close attention, including whether an independent third-party opinion has been obtained and how the pricing compares to recent market benchmarks. Third, the composition and independence of the oversight committee or advisory board play a vital role in mitigating conflicts of interest, as does the transparency of disclosure around any existing GP–LP dynamics that may influence the proposed transaction.

A thorough review must also consider the fund’s historical track record and the strategic rationale for retaining the asset rather than pursuing an outright sale. Investors should scrutinize the fee structure carefully, including management fees, any transaction-related costs, and the impact on carried interest calculations. Zaidwood Capital notes that evaluating the underlying financing terms is equally important, and our debt advisory team often helps clients analyze leverage arrangements embedded in continuation fund structures to ensure they align with long-term value-creation objectives. We also evaluate exit timing, market receptivity, and operational improvement plans to ensure the continuation path is realistic and achievable over time.

These due diligence pillars—alignment, valuation integrity, independent oversight, and fee transparency—form the foundation of informed LP decision-making in GP-led secondary transactions. With these best practices in mind, our team can assist in structuring and vetting such opportunities.

Key Takeaways and Next Steps in Continuation Fund Strategy

Our earlier sections laid out how private equity continuation funds serve as flexible structures that extend fund life and deliver intermediate liquidity. These vehicles allow general partners to hold prized assets longer while giving limited partners options to roll over or exit.

GP-led secondary transactions and single-asset continuation vehicles form the core of this strategy, aligning sponsor and investor interests through transparent pricing and governance. At Zaidwood Capital, we advise on structuring these transactions, from selecting the appropriate vehicle to managing the reinvestment process.

As you evaluate your next move, you may consider:

- Reviewing your current fund documents and limited partnership agreements for rollover provisions.

- Weighing single-asset continuation funds against multi-asset GP-led solutions based on your portfolio concentration and return objectives.

- Engaging a capital advisor experienced in secondary transactions and structured liquidity events.

Our Continuation Fund FAQ details common questions, and we invite you to book a discovery call for tailored guidance on your specific situation.

Resources

- Connect with Institutional LPs for Capital Formation

- Get Debt Advisory to Secure Growth Capital

- Find Debt Advisory to Fund Expansion Without Dilution

- Avoid Dilution with 2026 Debt Advisory Strategies

- Discover 2026 M&A Opportunities in Emerging Markets

- Get Comprehensive Guide to Private Equity Firms

- Access SEC Resources for Investor Protection

- Explore ICMA Standards for Capital Markets

- Get FINRA Investor Protection and Compliance Resources