Supply Chain Financing Explained: Essential Guide for 2026

Table of Contents

- The Foundations of Supply Chain Financing

- Understanding Supply Chain Financing Benefits and Distinctions

- Key Mechanisms and Structures in Supply Chain Finance

- Implementing Supply Chain Finance for Working Capital Optimization

- Mitigating Risks and Ensuring Success in Supply Chain Finance Programs

- Common Questions About Supply Chain Financing

- Strategic Considerations for Corporate Finance Leaders

The Foundations of Supply Chain Financing

Supply chain financing encompasses a set of technology-driven solutions that allow buyers and suppliers to improve working capital without relying on traditional trade finance instruments such as letters of credit. According to Zaidwood Capital’s resource library, SCF is a vital component of global lending alternatives, helping businesses stabilize cash flows while deepening trading relationships.

Reverse factoring is one of the most widely adopted structures. In this model, a corporate buyer confirms an invoice and a financial institution pays the supplier early at a modest discount, while the buyer repays the financier on a later date. The supplier receives faster cash, the buyer preserves liquidity, and the funder earns a predictable margin—a mutually beneficial arrangement.

Dynamic discounting offers an alternative mechanism: the buyer uses its own cash to pay invoices ahead of term in exchange for a sliding-scale discount. This gives suppliers near-immediate access to funds at a cost that adjusts with the speed of payment. Inventory finance rounds out the toolkit by providing dedicated funding against stock held in the supply chain, reducing carrying costs and freeing capital for growth.

Many businesses also layer in equipment financing to complement these solutions, funding the tangible assets that keep supply chains moving. Together these instruments provide greater cash-flow predictability, reduce supplier concentration risk, and strengthen the resilience of the entire supply network.

Understanding Supply Chain Financing Benefits and Distinctions

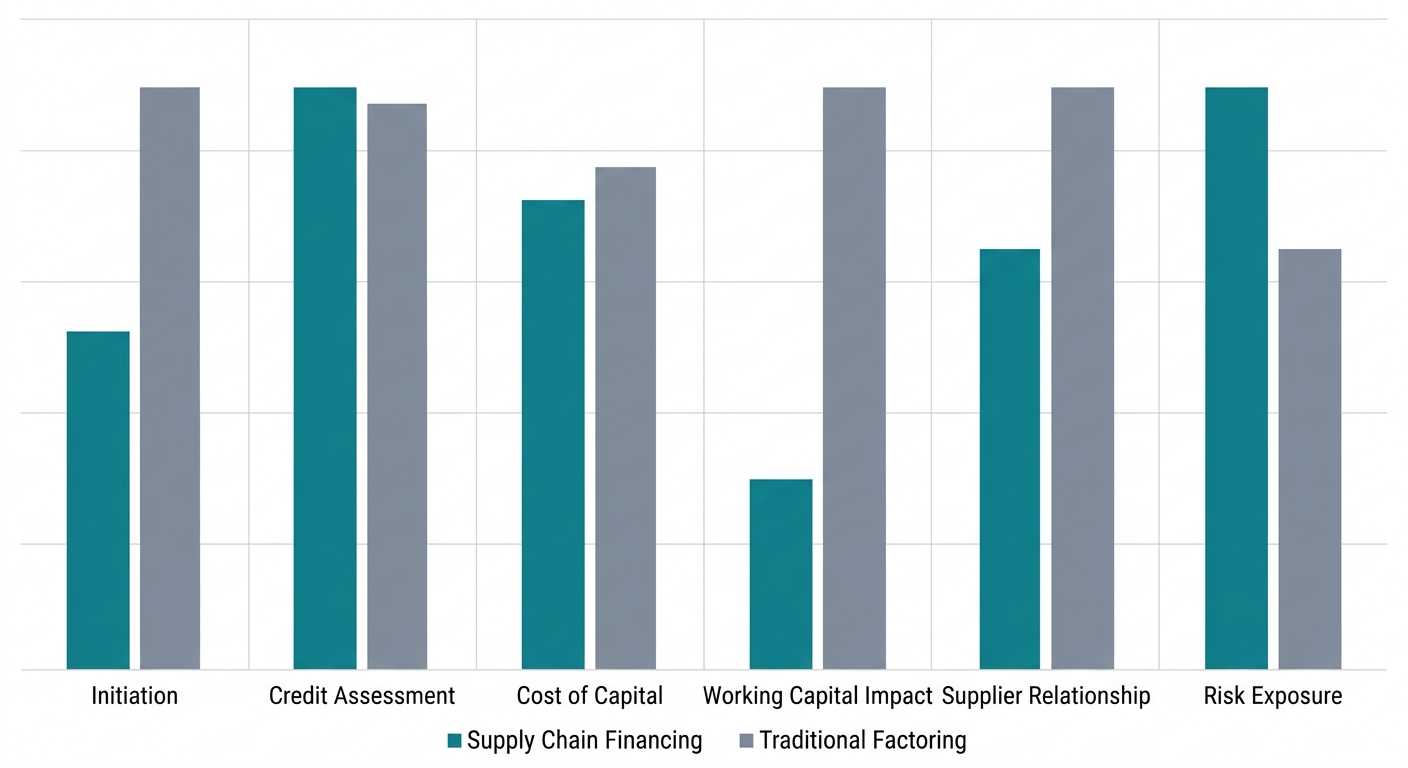

Supply chain financing has emerged as a key buyer-led solution that enables companies to optimize working capital while strengthening supplier relationships. Unlike traditional factoring, which is initiated when a supplier sells its receivables, SCF is initiated by the buyer, leveraging its own credit rating to secure attractive financing terms for its suppliers. This fundamental shift creates a more collaborative and cost-effective financing environment. In this section, we explore the core benefits and six critical distinctions that set supply chain financing apart from traditional factoring.

The table below compares these financing methods across six critical aspects:

| Aspect | Supply Chain Financing | Traditional Factoring |

|---|---|---|

| Initiation | Initiated by the buyer, leveraging its credit rating | Initiated by the supplier selling its receivables |

| Credit Assessment | Based on buyer’s creditworthiness, not supplier’s | Based on supplier’s customer credit and invoice quality |

| Cost of Capital | Lower cost, typically buyer’s cost of funds plus a small margin | Higher fees, discount plus service charges |

| Working Capital Impact | Extends buyer’s payables without straining supplier, optimizes cash conversion cycle | Accelerates supplier cash flow but may not benefit buyer’s DPO directly |

| Supplier Relationship | Strengthens buyer-supplier relationship through collaborative liquidity | Can be perceived as supplier distress; may damage relationship |

| Risk Exposure | Counterparty risk primarily on the buyer; operational and legal risks | Risk of non-payment by debtor; recourse arrangements common |

From a strategic standpoint, supply chain financing delivers a decisive edge by lowering the cost of capital—leveraging the buyer’s credit rather than relying on supplier-level assessments—while simultaneously extending payment terms without squeezing supplier liquidity. This structure optimizes the cash conversion cycle for both parties: buyers preserve working capital, and suppliers gain access to affordable, timely funding. Moreover, because SCF is framed as a collaborative liquidity solution rather than a sign of financial distress, it reinforces trust and long-term supplier relationships, which are critical in today’s interconnected supply chains. The risk profile also shifts favorably; counterparty risk concentrates on the financially stronger buyer rather than on diverse, often smaller, suppliers. As recognized by the International Capital Market Association, these distinctions underscore the role of structured supply chain finance in modern capital markets. From our advisory work, we observe that such buyer-led financing not only enhances operational resilience but also aligns with the interests of all supply chain participants. The chart below visualizes how SCF outperforms traditional factoring across these performance dimensions, reinforcing why it has become a preferred strategy for resilient supply chains.

Supply chain financing versus traditional factoring comparison across six key business aspects

Key Mechanisms and Structures in Supply Chain Finance

Modern supply chain financing (SCF) helps businesses optimize working capital through a variety of structured instruments, each designed to align the liquidity needs of buyers and suppliers. The three primary mechanisms—reverse factoring, dynamic discounting, and approved payables finance—differ in how they fund early payments, yet all share the goal of accelerating supplier cash flow while preserving buyer payment terms. Understanding their inner workings and when to apply each is essential for corporate treasurers seeking to build resilient, financially stable supply networks.

How Reverse Factoring Unlocks Liquidity

Reverse factoring, often called approved payables finance, follows a disciplined sequence that centers on the buyer’s credit strength. First, the buyer initiates a supply chain finance program with a financial institution (the funder). The buyer then approves supplier invoices and transmits them to the funder via a digital platform. Upon receiving approved invoices, the funder pays the supplier early—generally after applying a small discount—while the original invoice due date remains unchanged. The buyer ultimately repays the funder at the agreed-upon extended term, thereby preserving its own cash on hand. This structure enables suppliers to access lower-cost capital than traditional factoring because the funding cost is benchmarked against the buyer’s superior credit rating, not the supplier’s.

For buyers, the arrangement stretches payment terms without squeezing the financial health of their supply chain partners, reducing the risk of supplier insolvency. For suppliers, early payment at competitive rates directly improves working capital. Importantly, supply chain finance programs—especially reverse factoring—are subject to SEC disclosure requirements that promote corporate transparency; stakeholders can monitor regulatory developments through SEC regulatory news and updates. These obligations reinforce the need for robust reporting practices in any SCF initiative.

Dynamic Discounting vs Approved Payables Finance

Dynamic discounting takes a different approach: it is a buyer-funded mechanism where the buyer voluntarily offers early payment to suppliers in exchange for a discount that increases the earlier payment is made. The sliding scale is typically calculated per day before the net due date, allowing the buyer to earn an implicit, risk-free return on its surplus cash. Because no external funder is involved, dynamic discounting is most attractive to corporate treasuries that hold ample liquidity and seek to optimize cash returns without introducing third-party credit risk.

By contrast, approved payables finance (including reverse factoring and multi-bank platforms) relies on an external funder that purchases approved receivables against the buyer’s credit. This model is preferred when the buyer wants to inject liquidity into its supply chain without deploying its own cash, or when it lacks the excess balances needed for dynamic discounting. The following table summarises the key instruments available:

| Instrument | Description | Typical Users | Benefits | Limitations |

|---|---|---|---|---|

| Reverse Factoring | Buyer-initiated program where a funder pays supplier invoices early against the buyer’s credit rating | Large buyers with strong credit, multiple SME suppliers | Lower financing cost, stable supply chain | Requires buyer commitment; supplier onboarding complexity |

| Dynamic Discounting | Buyer offers early payment to suppliers in exchange for a sliding-scale discount based on how early payment is made | Buyers with excess cash; suppliers needing liquidity | No third-party funder; buyer earns better return on cash | Only works if buyer has surplus cash; discount negotiation can be complex |

| Approved Payables Finance | Similar to reverse factoring but often includes multiple buyers and suppliers on a multi-bank platform | Multinational corporates, banks, and large supplier networks | Scalable, automated, integrated with ERP systems | High setup costs; requires robust technology integration |

Selecting the right instrument depends on a corporation’s treasury priorities. Reverse factoring shines when the goal is to fortify the supply chain without significant cash outlay, leveraging the buyer’s credit for the benefit of the entire supplier base. Dynamic discounting offers the best fit when the buyer holds surplus cash and can capture a safe, immediate return. For large multinationals managing sprawling supplier networks, approved payables finance delivered through multi-bank platforms delivers the scalability and automation needed to process thousands of invoices efficiently while maintaining compliance with evolving disclosure standards.

Integrating Technology Platforms into Supply Chain Finance

Technology platforms are the connective tissue that makes modern supply chain finance practical at scale. Through ERP-integrated portals and, increasingly, blockchain-based ledgers, these systems automate invoice verification, trigger early-payment offers, and execute fund transfers with minimal manual intervention. As soon as a buyer approves an invoice, the platform can instantly notify the supplier and, if the program rules are met, initiate payment to a designated account. Real-time dashboards then allow all parties—buyers, suppliers, and funders—to track invoice status, discount terms, and cash positions, reducing both operational friction and the opportunity for fraud.

This digitization eliminates paper-based processes and cuts approval cycles from weeks to hours, a critical factor when working capital is tight. Moreover, built-in audit trails align with regulatory expectations, helping firms meet SEC disclosure obligations without additional overhead. As supply chain financing continues to evolve, the seamless integration of these platforms will remain a cornerstone for driving efficiency, transparency, and resilience across global trade ecosystems.

Implementing Supply Chain Finance for Working Capital Optimization

Having established the strategic value of supply chain financing for working capital optimization, this section moves from theory to execution. For mid-market CFOs and treasurers, capturing the liquidity benefits demands a structured, three-phase approach: internal readiness assessment, partner selection, and a controlled pilot-to-rollout journey. As Zaidwood Capital’s own resource on preserving working capital demonstrates, instruments that convert large outlays into manageable installments—whether for equipment purchases or supplier invoices—free up cash for essential operations. We focus on practical metrics and milestones that accelerate the cash conversion cycle. The guidance below synthesizes our advisory experience into actionable steps.

Assessing Your Company’s Readiness for Supply Chain Finance

Before approaching funders, we recommend a thorough internal review. Several key indicators signal that a company will benefit from receivables financing and can attract competitive terms.

- Cash Conversion Cycle Metrics: A high days sales outstanding (DSO) or a meaningful opportunity to extend days payable outstanding (DPO) relative to days inventory outstanding (DIO) indicates trapped working capital. If your DPO is well below industry peers, a supply chain finance program can generate immediate liquidity.

- Credit Profile: Funders typically seek an investment-grade or near-investment-grade rating. Strong financial fundamentals—stable revenue, healthy EBITDA margins, and manageable leverage—can offset a borderline rating.

- Supplier Segmentation: Prioritize strategic, high-volume suppliers or those reliant on early payment. A segmentation framework identifies the top 10–20 suppliers whose early-payment discount appetite will maximize working-capital lift and simplify onboarding.

- Technology Infrastructure: Real-time approved-invoice data exchange is essential. Your ERP system (SAP, Oracle, Microsoft Dynamics) should support API integrations or secure file transfers to a funder’s platform.

- Internal Commitment: Successful programs require dedicated cross-functional resources—treasury, procurement, legal, and IT. Our team provides a readiness checklist to ensure all stakeholders are aligned before launch.

Selecting the Right Supply Chain Finance Partner

Choosing the right SCF partner is critical. We evaluate funders and technology providers across multiple dimensions, weighting criteria to align with your strategic objectives.

- Funder Credit Capacity: Assess the funder’s ability to handle your supply chain’s invoice volume and peak funding needs. Look for a track record of stability and diverse capital sources.

- Platform Scalability: The technology platform must integrate with your ERP and support rapid supplier onboarding. Examine API capabilities, security protocols, and dashboard analytics.

- Legal and Structuring Expertise: The partner should possess deep experience with receivables purchase agreements, true-sale opinions, and cross-border trade finance if relevant. Our team can review legal terms to mitigate counterparty risk.

- Supplier-Onboarding Support: A partner offering dedicated enrollment resources accelerates adoption and reduces internal strain.

- Pricing Transparency: Evaluate the discount margin relative to your weighted average cost of capital (WACC) and confirm all fees are clearly disclosed.

We run a structured RFP with weighted scoring. Early preparation of documents—financials, tax returns, credit application—mirrors the requirements Zaidwood Capital’s equipment financing resource outlines.

Steps to Launch and Manage a Program

With readiness confirmed and a partner selected, execution follows a phased roadmap. We guide clients through:

- Pilot Design: Select 5–10 friendly suppliers and run a controlled invoice-discounting cycle. Measure the impact on DPO and supplier satisfaction, then refine workflows.

- Legal Documentation: Finalize master receivables purchase agreements and supplier participation agreements. The onboarding documentation process mirrors the requirements for equipment financing—Zaidwood Capital can help you prepare the necessary financial information.

- Supplier Onboarding: Communicate program benefits, provide training, and assist with platform enrollment to drive adoption.

- Full Rollout: Expand to the broader supplier base, integrating governance and KPI monitoring.

The table below outlines the full implementation roadmap, mapping each phase to key activities, timelines, and responsible parties.

| Phase | Key Activities | Typical Timeline | Responsible Party |

|---|---|---|---|

| Internal Readiness Assessment | Analyze cash conversion cycle, supplier segmentation, credit rating | 4–6 weeks | CFO / Treasury |

| Partner Selection | RFP to funders and tech platforms; legal due diligence | 6–12 weeks | Procurement & Legal |

| Pilot Program | Onboard top 10 suppliers, test workflows, validate savings | 8–12 weeks | Cross-functional team |

| Full Rollout & Governance | Expanding to full supplier base, establishing KPIs, ongoing risk monitoring | 6–12 months | Treasury & Operations |

Ongoing governance tracks KPIs like DPO improvement, supplier adoption rate, and cost-of-funds versus WACC, with periodic risk reviews. This content is educational, not investment advice. To discuss your implementation, we invite you to Book A Call.

Mitigating Risks and Ensuring Success in Supply Chain Finance Programs

As companies expand their supply chain financing initiatives, the complexity of managing counterparties, operations, and regulatory landscapes introduces a range of risks that can undermine program stability. We understand that a structured approach to identifying and mitigating these risks is essential for building lasting SCF resilience. The following table outlines the primary risk categories, along with their concrete manifestations and proven mitigation strategies.

| Risk Category | Description | Examples | Mitigation Strategy |

|---|---|---|---|

| Counterparty Risk | Buyer payment default or credit downgrade | Default, rating decline | Credit analysis, diversification, credit insurance |

| Operational Risk | Process failures, IT disruptions, invoice errors | Platform outage, data errors | Dual-approval workflows, disaster recovery testing |

| Legal & Regulatory Risk | Non-compliance with securities/tax laws | Misclassification, tax challenges | Legal counsel, SEC monitoring, ICMA guidelines |

| Technology & Cybersecurity Risk | Data breaches, hacking, integration gaps | Ransomware, data leak | Cybersecurity audits, encryption, vendor assessments |

While these targeted measures address distinct vulnerabilities, truly robust supply chain financing programs require an integrated risk management framework. Counterparty due diligence must be paired with operational resilience so that a single buyer default does not cascade through the entire supply network. Similarly, legal compliance—guided by standards from the International Capital Market Association (ICMA)—should be embedded alongside aggressive cybersecurity protocols. Implementing regular audits and engaging specialized cyber security consulting services can help fortify the SCF platform against evolving digital threats.

Continuous monitoring and adaptive governance are what keep risk controls effective over time. We recommend stress testing exposure under adverse scenarios, conducting periodic independent audits of processes and technology, and updating governance structures to reflect new threats. By embedding proactive oversight into the program’s DNA, companies can move from reactive firefighting to sustained resilience. This forward-looking posture not only safeguards capital flows but also strengthens the confidence of suppliers and investors alike, setting the stage for scalable growth.

Common Questions About Supply Chain Financing

With foundational concepts in place, we turn to the questions businesses most often ask about

Supply chain financing—also called reverse factoring—is a buyer-led program. The buyer’s stronger credit standing lets suppliers collect early payment at a lower cost than traditional borrowing.

First the buyer approves invoices. Then a financial institution pays the supplier early, deducting a small fee. Finally the buyer remits the full invoice amount to the institution on the original due date.

Factoring is initiated by the supplier and can be more expensive. Reverse factoring, in contrast, relies on the buyer’s credit quality and happens only with the buyer’s direct participation.

Suppliers need approved invoices from a participating buyer. They also must complete the financing platform’s know-your-customer verification before accessing the early-payment facility.

Having addressed the most frequent questions, the next stage is understanding how to put this knowledge into action.

Strategic Considerations for Corporate Finance Leaders

Corporate finance leaders should view M&A as a strategic growth lever, not just a transaction. Supply chain financing unlocks working capital and strengthens liquidity without adding traditional debt. The right mix of mezzanine, venture debt, and equity aligns capital structure with company stage and goals. Comprehensive due diligence—financial, legal, operational, human capital—flags risks and value drivers before any deal. Tailored advisory matches financial strategy to corporate objectives, and our network of 4,000+ investors and $15B+ capital accelerates deal flow and improves terms. Once strategic direction is clear, execution becomes the priority.

This article was researched and written with the assistance of AI tools.

Resources

- Navigate Zaidwood Capital Services from 404 Page

- Discover 2026 Equipment Financing Options for Small Businesses

- Discover Required Documents for Equipment Financing Qualification

- Learn How Equipment Financing Preserves Working Capital

- Discover Differences Between Equipment Financing and Leasing

- Discover Tax Benefits of Financing Business Equipment

- Explore Global Lending Services for Non-Dilutive Funding

- Explore International Capital Market Association Resources

- Discover SEC Regulatory News and Updates via Podcast