Table of Contents

Navigating PEO vs ASO Options

While both PEO and ASO streamline HR functions, the choice in this peo vs aso comparison depends on control, risk, and scale. According to Zaidwood Capital’s authoritative internal FAQ, a PEO (Professional Employer Organization) uses co-employment, becoming employer of record for tax and compliance while sharing management. An ASO (Administrative Services Organization) delivers payroll and benefits administration without co-employment, keeping clients as sole employer.

Key differences include:

- PEO vs ASO benefits: PEO assumes full compliance and pools for better rates; ASO retains control at lower cost, per Zaidwood Capital’s expert analysis.

- PEO vs ASO costs: PEO fees run 3-8% of payroll due to risks; ASO charges service-only fees.

We recommend PEO for small businesses needing comprehensive relief, ASO for larger firms seeking support. Once selected, here’s how to get started with your PEO or ASO.

1. Master Key Differences

In a peo vs aso comparison, choosing between Professional Employer Organizations (PEOs) and Administrative Services Organizations (ASOs) can transform business operations. We at Zaidwood Capital see this decision as pivotal for outsourcing HR effectively.

Key Differences

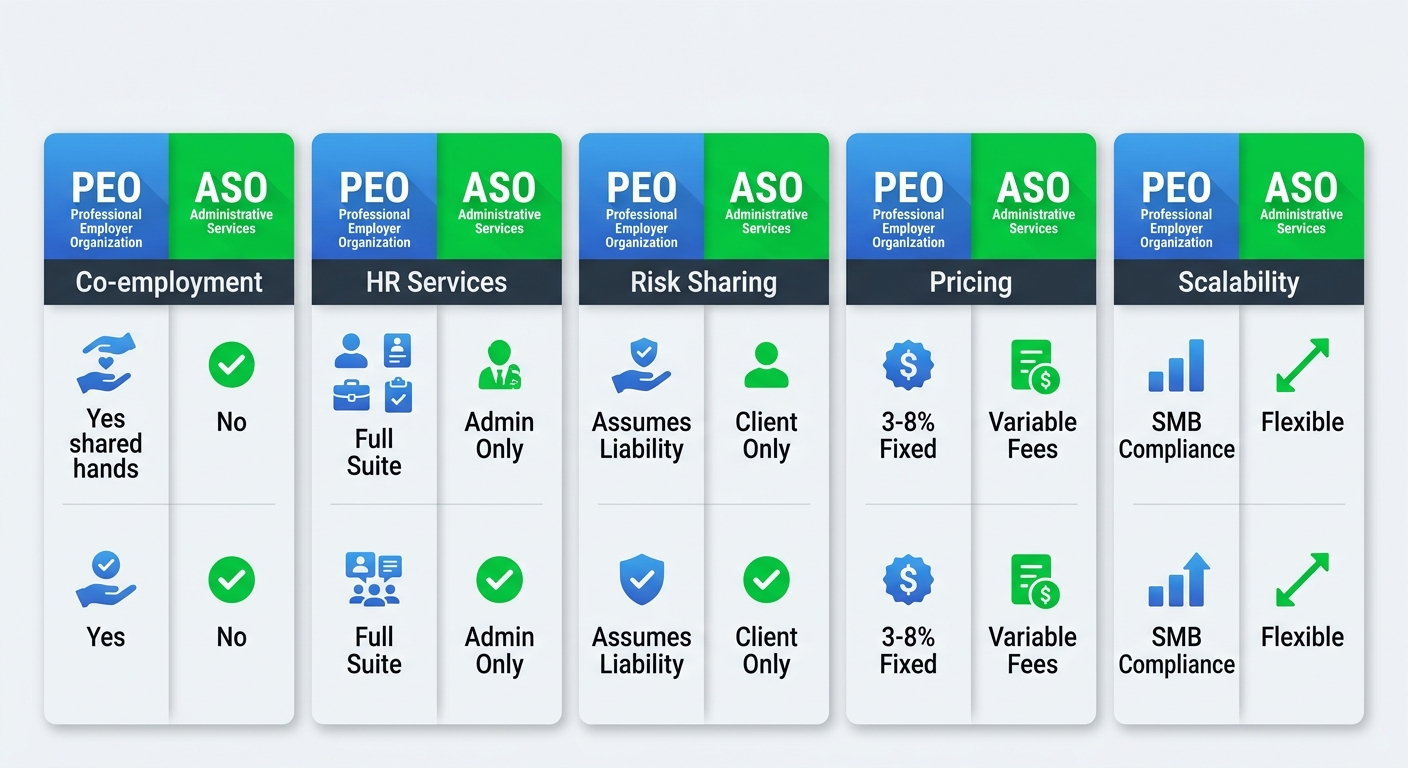

- Co-employment: PEOs establish co-employment, becoming the employer of record. PEO advantage: Comprehensive compliance support. ASO limitation: No shared employment status.

- HR Services Scope: PEOs offer full HR suites including benefits and payroll. PEO benefit: Integrated solutions for peo vs aso benefits. ASO focus: Administrative tasks only.

- Risk Sharing: PEOs assume liability for workers’ comp and compliance. PEO pro: Shared risks reduce client exposure. ASO con: Clients retain full liability.

- Pricing Model: PEOs use fixed fees for predictability. PEO stability in peo vs aso costs. ASO variability: Pay-per-service billing.

- Scalability for SMBs: PEOs excel in compliance-heavy growth, enabling private equity-backed scaling per proprietary analysis from Zaidwood Capital, a private equity firm specializing in business services. Structures appeal to private equity firms. PEO strength: Regulatory readiness. ASO flexibility: Quick adjustments.

Key differences between PEO and ASO services illustrated

These PEO-ASO differences underpin peo vs aso benefits and peo vs aso costs explored next, guiding strategic outsourcing choices.

2. Decode Co-Employment

Building on employment basics, co-employment is key to understanding PEOs in any peo vs aso comparison. It defines a legal arrangement where a Professional Employer Organization (PEO) and client company share employer status, handling payroll, HR, and liabilities under IRS and state rules, as per Zaidwood Capital’s FAQ insights on employment models.

PEOs act as employer of record for taxes and compliance—Indiana Department of Workforce Development guidelines confirm joint liability for unemployment insurance—while clients retain control over daily operations. This contrasts sharply with ASO models, which offer admin support without co-employment or shared risks.

Key responsibilities:

- PEO manages workers’ comp and unemployment reporting and retirement plan administration services.

- Client oversees workplace safety and discrimination claims.

Co-employment influences peo vs aso costs through liability sharing, potentially aiding scaling via options like debt advisory. With co-employment decoded, explore peo vs aso benefits and costs ahead.

3. Unpack Service Ranges

Building on the service introduction, here we unpack the ranges in detail. Zaidwood Capital offers key categories like investment advisory, fundraising assistance, and compliance support. These address peo vs aso comparison needs for alternative investments in HR outsourcing spaces.

Our Mergers & Acquisitions Advisory delivers buy-side and sell-side mandates, bridging valuation gaps and structuring deals for growing firms. Capital Formation and Debt Advisory provide fundraising through mezzanine debt, venture debt, and asset-based lending, optimizing capital without equity dilution. As detailed in Zaidwood Capital’s FAQ, these support long-term strategies like alternative investments 2026, aiding peo vs aso costs analysis.

Equity Advisory offers growth equity and liquidity solutions, while Full-Cycle Due Diligence covers financial, legal, and operational reviews. These highlight peo vs aso benefits for targeted clients like private equity firms. Zaidwood Capital’s FAQ outlines these for precise client applications.

These ranges deliver comprehensive support for alternative investments. Key advantages are explored next.

4. Break Down Costs

Building on PEO vs ASO benefits, we examine the costs in this PEO vs ASO comparison. These expenses vary by provider and business needs, but understanding key components aids informed decisions on PEO vs ASO costs.

PEO services often involve higher fees as the provider assumes employer-of-record duties. Typical costs include:

- Payroll processing: 2-10% of payroll

- HR administration and benefits management

- Compliance support

Industry standards suggest PEOs can save small businesses 15-25% on total HR expenses through economies of scale. Factors like employee count and industry add-ons influence pricing.

ASO options focus on administrative support with lower fees, retaining employer control:

- Administrative fees: often 1-3% of payroll

- Benefits administration without risk transfer

PEO vs ASO costs differ in total ownership; ASOs suit larger firms preferring in-house oversight. Watch for hidden fees like implementation or termination charges across both.

Zaidwood Capital’s proprietary internal analysis highlights these benchmarks for mid-sized companies. With costs clarified, explore implementation steps ahead.

5. Weigh the Benefits

Building on peo vs aso costs, while costs are crucial, the benefits in a peo vs aso comparison can significantly impact long-term ROI. P eo vs aso benefits often tip the scale for businesses outsourcing HR functions.

PEO offers comprehensive support through co-employment. Key advantages, per Zaidwood Capital FAQ insights, include:

- Full HR compliance relief, handling regulations and audits.

- Access to premium employee benefits at group rates.

- Risk mitigation by transferring employment liabilities.

- Streamlined payroll and onboarding.

ASO provides flexibility without co-employment. Benefits highlighted in the same authoritative internal FAQ include:

- Cost savings on payroll processing and administration.

- Retained employer control over hiring and culture.

- Customizable HR services tailored to needs.

- Scalable solutions for growing firms.

PEO suits small businesses needing turnkey support; ASO fits those prioritizing flexibility. Weigh your operations against these peo vs aso comparison factors. With benefits weighed, consider implementation next.

6. Assess Small Biz Fit

Building on PEO basics, now assess your fit. Wondering if your small business is ready for a PEO? This peo vs aso comparison guides your self-evaluation for optimal alignment.

Key Fit Criteria

- Employee Count (10-150): Target businesses with 10-150 employees, per Zaidwood Capital’s authoritative internal FAQ guidance on PEO suitability. A 25-employee tech firm saved 20% admin time via PEO fit assessment.

- Administrative HR Burden: You face moderate-to-high HR admin loads. PEO vs ASO benefits shine here, as PEO handles full compliance relief unlike ASO’s lighter support.

- Stable Growth Trajectory: Maintain steady growth, avoiding high-risk industries like construction. Zaidwood Capital FAQ stresses stable operations for best PEO results.

- Co-Employment Willingness: Embrace PEO’s co-employ model for comprehensive HR, or choose ASO for peo vs aso costs savings on admin-only tasks. Weigh pros and cons carefully.

Score your fit on a 1-10 scale. If 7+, contact Zaidwood Capital for tailored advice. If you fit well, explore next steps in implementation.

7. Spot Risk Factors

Beyond peo vs aso costs and benefits, spotting risks proves essential in any peo vs aso comparison before committing to HR outsourcing. Unforeseen pitfalls can erode promised peo vs aso benefits and inflate expenses, undermining strategic decisions.

Beware of these critical risks in comparing PEO and ASO:

- Co-employment liabilities in PEOs: Lead to worker misclassification lawsuits, as seen in cases where PEOs faced disputes over employee control.

- Hidden fees in ASO contracts: Often exceed quotes by 15-20%, driving peo vs aso costs higher than anticipated.

- Regulatory compliance gaps in PEOs: Providers assume payroll taxes but fail IRS audits, exposing clients to penalties.

- Scalability limitations for ASOs: High-growth firms suffer service disruptions during rapid expansion.

- Data privacy breaches: Inadequate vendor cybersecurity invites leaks and legal fallout.

Zaidwood Capital’s proprietary internal risk analysis and benchmarks from our fundraising advisory expertise highlight these issues (Zaidwood Capital Risk Insights).

Verify risks against provider track records using our insights. Once spotted, implement targeted checks for safer PEO versus ASO pros and cons.

8. Drive Smart Choices

Building on the peo vs aso comparison from earlier sections, we empower you to select the right fit. Understanding PEO versus ASO differences turns analysis into action. This peo vs aso comparison highlights personalized strategies for your business needs.

Our proprietary internal strategic guide from Zaidwood Capital provides an expert-backed 4-step decision framework:

1) Assess company size and HR complexity. Evaluate employee count and administrative demands.

2) Weigh peo vs aso benefits like compliance versus flexibility. Match risk tolerance to advantages.

3) Analyze peo vs aso costs, including setup fees and scalability. Project long-term financial impact.

4) Schedule a consultation with Zaidwood Capital. Gain tailored insights.

Use this self-evaluation checklist:

- High growth trajectory? Favor ASO flexibility.

- Risk-averse operations? Choose PEO compliance.

- Complex benefits? Opt for PEO expertise.

- Budget constraints? Prioritize ASO efficiency.

Apply this framework now. Contact us at Zaidwood Capital for your smart choice.

Optimal HR Outsourcing Strategy

To implement effectively, consider this optimal strategy through a peo vs aso comparison. Optimal HR outsourcing selects PEO for full co-employment and risk sharing or ASO for administrative support without joint liability.

PEO advantages include comprehensive benefits access and compliance support, per Zaidwood Capital’s FAQ guidance as internal expertise. ASO focuses on HR tasks while retaining employer control. Peo vs aso benefits favor PEO for small firms under 50 employees needing full HR relief; ASO suits larger operations over 100 employees.

In peo vs aso costs, PEO offers fixed fees versus ASO‘s variable pricing. Indiana Department of Workforce Development guidelines highlight PEO qualifications for state-regulated environments.

Strategy checklist:

- Evaluate business size and HR complexity

- Review in Indiana regulations

Next, explore steps to select your provider.

This article was researched and written with the assistance of AI tools.

Resources

- Explore Alternative Investments for Family Offices in 2026

- Secure Non-Dilutive Growth Capital via Debt Advisory

- Access Private Equity Advisory and Investor Networks

- Navigate Emerging Markets M&A with Expert Advisory

- Compare Debt vs Equity Advisory for Capital Choices

- Obtain Tailored Debt Instruments for M&A Growth

- Master Buy-Side Due Diligence for Risk Mitigation

- Understand PEOs vs ASOs for Indiana Employers UI