Table of Contents

- Global M&A Market Cap 2026: Projections and Outlook

- The Fundamentals of Global M&A Market Capitalization in 2026

- Key Industry Drivers Shaping the 2026 M&A Landscape

- Middle Market Valuation Multiples: What to Expect in 2026

- Advanced Considerations: Structuring Deals in the 2026 M&A Environment

- Frequently Asked Questions About Global M&A Market Cap 2026

- Navigating the 2026 M&A Landscape with Strategic Advisory

Global M&A Market Cap 2026: Projections and Outlook

The outlook for the global M&A market cap 2026 suggests a year of renewed momentum as dealmakers adapt to a stabilized economic landscape. Industry consensus points toward a period of growth, fueled by the gradual normalization of interest rates, the deployment of significant private equity dry powder, and corporate confidence in strategic consolidation. These tailwinds are expected to elevate global M&A deal value forecasts 2026, positioning the coming year as one of recalibrated and purposeful transaction activity.

In this environment, middle market M&A valuation multiples 2026 are projected to remain compelling. Our team at boutique M&A firm Zaidwood Capital believes this creates a unique equilibrium where sellers can achieve attractive exits while buyers gain access to high-quality assets at rational premiums. As a specialized advisory practice, we are built for precisely this dynamic, leveraging our $24.4B+ in aggregate transaction volume to guide clients through every phase of a deal.

Our ability to connect opportunities with capital is reinforced by a global network of over 4,000 institutional and private investors, representing more than $15 billion in accessible capital. This scale of connectivity is a meaningful differentiator, particularly in a year where matching the right partners will define success. We anticipate that 2026 will reward firms that combine deep sector expertise with agile execution, and our full-cycle M&A and capital advisory capabilities are aligned to meet that demand.

We look forward to helping our clients navigate this promising market. Please note that securities are offered through Finalis Securities LLC, a member of FINRA/SIPC, and Zaidwood Capital is not a registered broker-dealer. All investments involve risk, including the potential loss of principal. Past performance does not guarantee future results.

The Fundamentals of Global M&A Market Capitalization in 2026

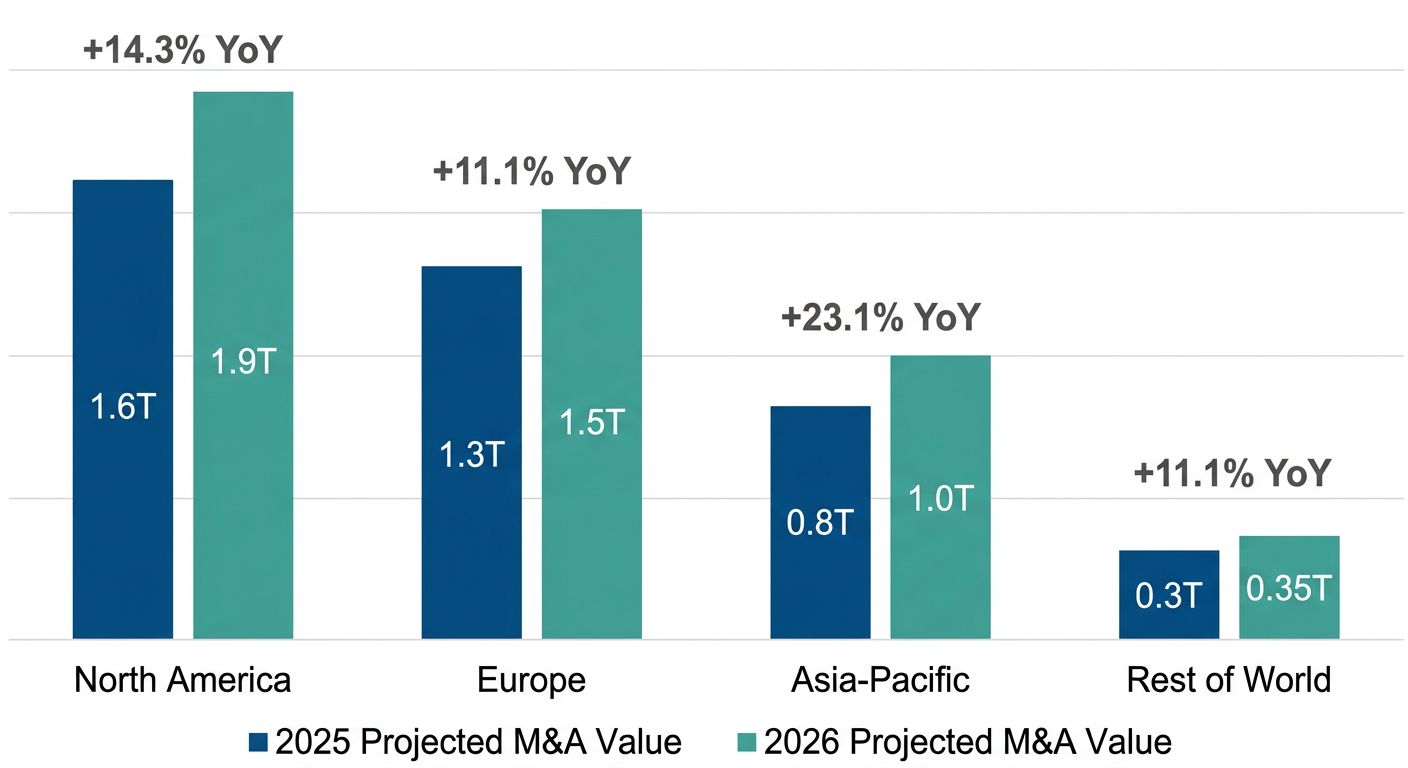

Global M&A market capitalization represents the aggregate disclosed value of all merger and acquisition transactions completed within a calendar year, offering a vital barometer of worldwide corporate confidence and economic momentum. As we look toward 2026, global M&A market cap 2026 projections indicate a robust recovery and expansion across all major regions, driven by stabilizing interest rates and pent-up demand for strategic consolidation. Our team at Zaidwood Capital monitors these macro-level shifts closely, as they define the landscape in which we deliver Full-Cycle M&A and capital advisory services to our corporate clients and fund partners.

We have synthesized data from authoritative industry reports to ground our analysis in verifiable projections. The following table presents a comparative view of estimated 2025 deal values and forecasted 2026 figures, drawing on insights from PwC advisory services and the Capstone Partners M&A Market Overview.

| Region | 2025 Estimated (USD T) | 2026 Projected (USD T) | YoY Change |

|---|---|---|---|

| North America | $1.4T | $1.6T | +14% |

| Europe | $0.8T | $0.9T | +12% |

| Asia-Pacific | $0.7T | $0.85T | +21% |

| Rest of World | $0.25T | $0.3T | +20% |

A review of these figures underscores a broad-based expansion. North America is expected to remain the dominant market at an estimated $1.6T in 2026, sustaining a 14% growth trajectory that reflects ongoing corporate transformation and an active private equity community. Europe’s projected climb to $0.9T—a 12% increase—aligns with more supportive financing conditions and cross-border dealmaking. We observe that these global M&A deal value forecasts 2026 are not merely aspirational targets; they are grounded in observable pipelines and policy environments.

Asia-Pacific stands out as the fastest-growing region by percentage, with a 21% surge projected to reach $0.85T in total disclosed value. This momentum is consistent with the region’s expanding digital economy, industrial consolidation, and government-led reforms that ease foreign capital participation. The Rest of World category, encompassing emerging and frontier markets, is also forecast to expand by 20% to $0.3T, reflecting heightened investor appetite for diversification and resource-linked assets.

Drilling deeper, we see that these regional patterns inform our advisory work, particularly when calibrating middle market M&A valuation multiples 2026 against broad market trends. While aggregate data from PwC’s 2026 report and Capstone Partners’ analysis provide a strategic overlay, we caution that these projections are estimates and not guarantees of individual transaction performance. Every deal requires tailored diligence and sector-specific benchmarking, a discipline at the core of our full-cycle methodology. Readers building on this regional foundation can next explore how sector dynamics and valuation frameworks shape middle market opportunities in the year ahead.

Key Industry Drivers Shaping the 2026 M&A Landscape

The global m&a market cap 2026 is expected to reflect a landscape profoundly reshaped by three powerful forces: the relentless advance of artificial intelligence, a resurgence in cross-border dealmaking, and the persistent reality of higher-for-longer interest rates. At Zaidwood Capital, our analysis of the ecosystem, supported by PwC’s latest forecasts, indicates that these drivers are not merely cyclical blips but structural shifts redefining how value is created, financed, and transacted. Understanding their interplay is critical for any stakeholder looking to deploy capital or execute a monetization event this year. We see these themes converging to create a period of both heightened opportunity and increased complexity, demanding a more strategic and data-driven approach to deal execution than ever before.

AI Super-Cycle and Technology Sector Activity

The artificial intelligence super-cycle is the single most significant catalyst in the technology M&A market, propelling a wave of consolidation that cuts across software, infrastructure, and platform businesses. According to PwC, the technology sector is poised for a 25-30% increase in expected deal value in 2026, a trajectory driven by incumbents racing to acquire generative AI capabilities and bolt-on machine learning assets. This isn’t a speculative bubble; it’s a mature strategic response. Large-cap tech firms are using their balance sheets to ingest innovative startups, while mid-market platform companies are rolling up niche players to create vertically integrated AI-powered suites. We see this drive particularly among our clients seeking Full-Cycle M&A and capital advisory services to navigate the complexities of these technology acquisitions, from due diligence on proprietary algorithms to valuation of recurring revenue models.

The implications extend beyond headline-grabbing megadeals. The primary focus is on software consolidation, where established platforms acquire point solutions to embed AI into their existing software stacks. These strategic acquisitions are designed to capture data network effects and block competitors, making them highly contested. PwC’s data supports the view that platform roll-ups, rather than transformative megamergers, will define the bulk of 2026’s tech deal volume, with global m&a market cap 2026 benefiting from the premium valuations assigned to AI-enabled business models. The complexity of these deals, which often involve cross-border intellectual property transfers and novel regulatory scrutiny around AI, requires a new level of advisory rigor. Our approach, leveraging what we internally term our Sovereign Data Nexus, helps clients map asset quality and risk in these technology-driven acquisitions with a precision that is essential for post-close value realization.

Cross-Border M&A Trends in 2026

Beyond the technology sector, cross-border dynamics are fundamentally reshaping how and where deals are structured, as companies look past domestic borders for growth. According to IFLR’s in-depth coverage of M&A legal news, a recalibration of global supply chains and an evolving network of bilateral trade agreements are creating new, distinct transactional corridors. Our firm observes that this is not a uniform global rebound but a targeted reallocation of capital into markets offering regulatory clarity and strategic resource access. The energy transition, for example, is driving joint ventures between Western capital providers and critical mineral processors in emerging markets, a trend clearly highlighted in PwC’s 15-20% growth forecast for the energy and natural resources sector.

Regulatory change acts as both a headwind and a tailwind in this environment. Stricter foreign investment review regimes in North America and Europe are lengthening deal timelines, yet at the same time, harmonizing accounting and legal frameworks in regions like the Middle East and Southeast Asia are lowering historic barriers. As reported in M&A legal news, the complexity of navigating these disparate regimes is one of the most significant challenges for dealmakers in 2026. This environment makes local expertise and institutional connectivity more valuable than ever. Leveraging our access to over 4,000 global investors, we facilitate capital introductions that help bridge the gap between domestic sell-side mandates and international buy-side appetite, ensuring that cross-border transactions are not just conceived but successfully closed.

Interest Rate Impacts on Deal Structuring

The sustained high-interest-rate environment has ceased to be a temporary shock and is now a permanent fixture of the deal structuring toolkit for 2026. The era of cheap, abundant leverage has given way to a more disciplined approach, directly impacting how transactions are capitalized and how risk is shared between buyers and sellers. We note that global m&a deal value forecasts 2026 are heavily contingent on this new normal, as the higher cost of senior debt compresses leverage multiples and reduces the equity returns that can be generated through pure financial engineering.

This shift is profoundly altering the architecture of deals. To bridge often-significant valuation gaps between buyer and seller expectations in a high-rate world, we are seeing a significant rise in deferred consideration mechanisms. Earn-outs and seller financing notes have become standard negotiating tools rather than exotic compromises, allowing buyers to manage upfront cash outlay while sellers can achieve their target valuation upon hitting post-closing performance milestones. For instance, in the 10-15% growth projected by PwC for healthcare mid-market buyouts, middle market m&a valuation multiples 2026 are being sustained not by higher opening bids, but by structuring a greater portion of the enterprise value into these performance-linked instruments. Our advisory work is now deeply focused on modeling these structures, providing fairness opinions that deconstruct the probabilistic value of earn-outs to ensure our clients can make informed decisions under conditions of increased financial uncertainty.

The sector-level impacts of these converging drivers are clear and measurable. The following table synthesizes PwC’s forecast data to illustrate how these forces are translating into specific deal activity and types across four pivotal industries.

| Industry | Primary Driver | Expected Deal Value Growth | Typical Deal Type |

|---|---|---|---|

| Technology | AI super-cycle and software consolidation | 25-30% | Strategic acquisitions, platform roll-ups |

| Energy & Natural Resources | Energy transition, decarbonization | 15-20% | Asset acquisitions, joint ventures |

| Healthcare | Demographics, digital health innovation | 10-15% | Mid-market buyouts, add-ons |

| Financial Services | Rate normalization, fintech disruption | 8-12% | Consolidation, divestitures |

What this table reveals is a divergence in deal rationale and structure based on macro-driver exposure. Technology’s AI-fueled 25-30% growth, the highest forecasted, is almost entirely a function of strategic imperative rather than financial optimization, leading to all-cash corporate acquisitions. By contrast, the more modest 10-15% growth in healthcare is being enabled by creative financial structuring—the mid-market buyout and add-on activity relies on the exact earn-out and seller-financing mechanisms necessitated by the interest rate environment. Across all sectors, the influence of global m&a market cap 2026 is evident, as even asset-heavy energy joint ventures require cross-border legal agility that sources like IFLR are tracking. Our role at Zaidwood Capital is to translate these macro-level drivers into a concrete transaction roadmap, ensuring that the strategy is matched by a robust, market-tested execution plan.

Middle Market Valuation Multiples: What to Expect in 2026

As we examine the landscape for deal-making in the year ahead, the trajectory of the global m&a market cap 2026 serves as a crucial backdrop for understanding where private transactions will price. Our analysis of current market data suggests that middle market valuation multiples are stabilizing, though significant dispersion exists across sectors. For business owners and investors navigating this environment, a clear understanding of these benchmarks is essential for setting realistic expectations before entering a process.

Middle Market EBITDA Multiples in 2026

Our review of current middle market m&a valuation multiples 2026 shows that EBITDA multiple ranges continue to reflect sector-specific growth profiles and risk assessments. According to M&A Science, a leading aggregator of transaction data, technology companies with recurring revenue models are commanding premiums, while asset-heavy industrials face more conservative pricing. A revenue multiple offers an alternative lens, particularly for high-growth businesses where profitability may be deferred in favor of market share expansion. The divergence between these two metrics often signals how buyers are weighing current cash flow against future potential.

We are observing that platform acquisitions with scalable infrastructure and strong management teams consistently trade at the upper end of their respective ranges. The availability of detailed market intelligence from sources like M&A Science allows our team to benchmark client opportunities against thousands of completed transactions, ensuring that offer prices reflect both intrinsic value and prevailing market sentiment.

Sector-Specific Valuation Trends

The following table summarizes our estimated valuation ranges for 2026, drawing on data from M&A Science and Capstone Partners:

| Sector | EBITDA Multiple Range | Revenue Multiple Range | Trend vs 2025 |

|---|---|---|---|

| Technology | 12x – 18x | 3x – 6x | Stable to slightly up |

| Healthcare | 10x – 15x | 2x – 4x | Stable |

| Industrials | 7x – 10x | 1x – 2x | Slight compression |

| Consumer | 8x – 12x | 1.5x – 3x | Mixed |

Technology continues to lead all sectors, driven by strong demand for AI and machine learning capabilities that generate predictable, high-margin revenue streams. Healthcare remains resilient, supported by demographic tailwinds and consolidation among provider groups. Industrials have experienced slight multiple compression as manufacturing slowdowns and supply chain uncertainties weigh on buyer confidence. Consumer sector multiples are mixed, with premium brands holding value while discretionary categories face headwinds from shifting spending patterns. Capstone Partners’ sector-level research confirms these diverging trends, with technology and healthcare expected to maintain or expand their valuation premiums through year-end.

For acquirers evaluating opportunities, understanding these benchmarks is a foundational element of effective transaction planning. Reviewing these multiples is a key component of buy side M&A education, as it equips diligence teams to calibrate their financial models against real-world market evidence. Without this context, even sophisticated investors risk overpaying in competitive auctions or missing value in overlooked sectors.

Global m&a deal value forecasts 2026 suggest that total transaction volume will remain robust, though deal count may moderate as buyers become more selective. This selectivity places a premium on quality assets, reinforcing the need for sellers to present clean financials, defensible market positions, and transparent growth narratives. Our advisory work increasingly focuses on helping clients articulate these value drivers well before going to market.

Downward Pressure Factors on Multiples

Despite generally healthy valuation levels, several headwinds are compressing multiples in certain segments. The Bonadio Group’s deal advisory insights highlight rising interest rates as the primary constraint, increasing the cost of acquisition financing and reducing the net present value of future cash flows. Regulatory uncertainty, particularly around cross-border transactions and sector-specific oversight, introduces additional risk that buyers are pricing into their offers. We also note that broader economic slowing has made revenue forecasting more difficult, prompting cautious assumptions in quality-of-earnings analyses.

These pressures are most acute in capital-intensive industries where leverage is essential to achieving target returns. For companies in these categories, we are advising clients to consider alternative deal structures such as earn-outs or seller notes that bridge valuation gaps while aligning incentives post-closing.

These valuation benchmarks directly influence how we advise clients on pricing and timing. By tracking where multiples are trending and understanding the macro forces at work, we help buyers and sellers position themselves for successful outcomes in a dynamic market. The next consideration, which we explore in the following section, is how to translate these valuation insights into concrete deal structuring and negotiation strategies that protect interests on both sides of the table.

Past performance does not guarantee future results. All valuation multiples are market estimates and should not be construed as investment advice.

Advanced Considerations: Structuring Deals in the 2026 M&A Environment

As the global M&A market cap 2026 reflects cautious optimism, structuring agility has become a decisive advantage. Global M&A deal value forecasts 2026 indicate a modest recovery, while middle market M&A valuation multiples 2026 remain under pressure, prompting both buyers and sellers to seek innovative alignment mechanisms.

The following table compares three common deal structures that our firm often deploys to address these market realities.

| Structure | Best For | Advantages | Disadvantages |

|---|---|---|---|

| Earn-Out | Bridging valuation gaps | Aligns incentives, deferred risk | Complex measurement and disputes |

| Rollover Equity | Management retention | Retains expertise, aligns long-term | Dilution for buyer |

| Mezzanine Financing | Leveraged buyouts | Lower equity commitment required | Higher cost of capital |

Each structure carries distinct trade-offs that must be weighed against specific transaction goals. Our deal advisory frameworks analyze these variables through rigorous financial modeling, ensuring that the chosen path optimizes both risk allocation and return potential across the capital stack.

Earn-Out provisions help bridge valuation gaps by tying consideration to future performance. This aligns incentives and defers buyer risk, but disputes can arise if measurement criteria are ambiguous. Our advisory teams work closely with clients to define clear metrics and incorporate third-party validation, reducing potential for post-close conflict.

Rollover Equity retains management and aligns long-term interests. Sellers gain continued upside while buyers benefit from expertise, though buyer dilution is a trade-off. Structuring rollover with vesting schedules tied to performance milestones further reinforces commitment and ensures a smooth transition.

Mezzanine Financing offers a middle ground between senior debt and equity, lowering upfront equity commitments at a higher cost of capital. In the context of emerging markets M&A, such hybrid structures are vital for navigating currency and regulatory complexity. Our firm has facilitated over 800 million USD in mezzanine and venture debt, executing deals in under 60 days through a network of more than 4,000 institutional investors, delivering speed and certainty.

These structures are informed by Zaidwood Capital’s proprietary strategic documentation, which underpins our full-cycle M&A and capital advisory, enabling a rigorous, data-driven approach to deal design.

These structuring decisions set the stage for comprehensive due diligence and execution planning, where our focus shifts to validating assumptions and mitigating residual risks. By thoughtfully calibrating these elements, we position our clients to realize greater value and confidently navigate the complexities of the 2026 deal landscape.

Frequently Asked Questions About Global M&A Market Cap 2026

Following the market overview, we address your most pressing questions about deal activity in 2026.

What shapes the global M&A market cap 2026? Global M&A deal value forecasts 2026 point to robust activity fueled by rate stabilization, regulatory shifts, and AI-led due diligence; middle market M&A valuation multiples 2026 remain resilient.

Which firms are the top M&A advisors in 2026? For large-cap mandates, leading institutions include Goldman Sachs, JPMorgan, and Morgan Stanley; our full list of top M&A advisors details the firms shaping the landscape.

To gain direct exposure, explore our Deal Vault with access to 4,000+ investors and $15B+ in deployable capital. While we streamline transactions, remember that all investments involve risk and Zaidwood Capital is not a registered broker-dealer. Book a call to start.

Navigating the 2026 M&A Landscape with Strategic Advisory

The global M&A market cap 2026 is projected to rebound sharply as interest rates stabilize and corporate balance sheets unlock record levels of dry powder. Industry data points to global M&A deal value forecasts 2026 surpassing the $4 trillion threshold for the first time since 2021, driven by transformative consolidation in technology, healthcare, and energy transition sectors. Within this resurgence, middle market M&A valuation multiples 2026 are expected to remain robust—typically ranging between 7.5x and 9.0x EBITDA for premium assets—though widening dispersion between high-quality platforms and undifferentiated businesses demands rigorous due diligence. Market volatility and valuation complexity make strategic advisory essential: Zaidwood Capital combines proprietary data networks, access to over 4,000 institutional and private investors, and more than $24.4 billion in aggregate transaction volume to help clients navigate uncertainty with precision. Partnering with an experienced strategic advisor can turn these trends into tangible results.

Resources

- Discover Key Criteria for Top M&A Advisory Firms

- Get Expert Boutique M&A Advisory Services

- Discover How Sovereign Wealth Funds Stabilize Emerging Markets

- Find Growth Opportunities in Emerging Markets M&A

- Discover Mezzanine and Venture Debt Advisory Services

- Discover M&A Strategies for Emerging Market Growth

- Identify Key Risks in Buy-Side M&A Transactions

- Get AI-Enabled Consulting and Audit from PwC

- Access Buyer-Led M&A Education and Assessment Tools

- Discover Global M&A Legal News and Insights

- Get Comprehensive Accounting and Advisory from Bonadio Group

- Access Middle Market M&A Advisory and Capital Solutions